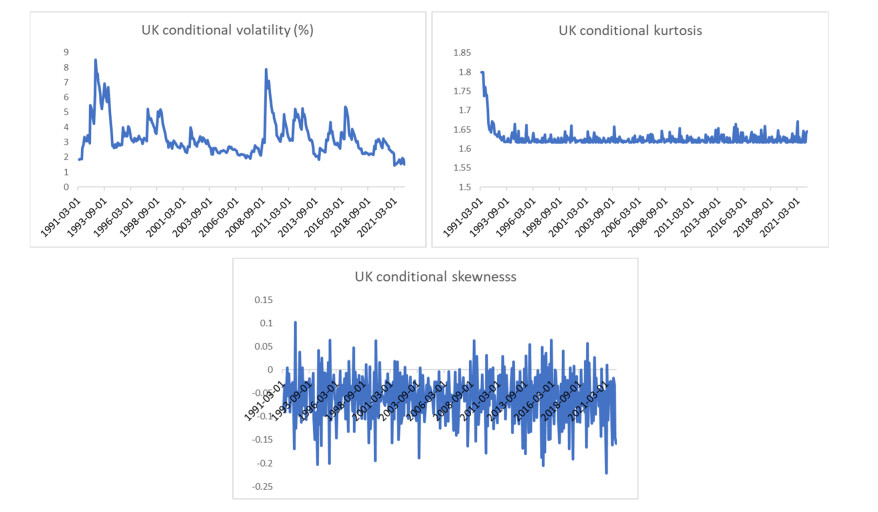

We analyze the risk-return trade-off for international (France, Germany, Netherlands, Spain, UK, and US) government bond markets and the US stock market. We measure risk by the higher order moments (volatility, skewness, and excess kurtosis) as they are defined in

Citation: Charlotte Christiansen, Christos S. Savva. Government bond market risk-return trade-off[J]. Quantitative Finance and Economics, 2023, 7(2): 249-260. doi: 10.3934/QFE.2023013

We analyze the risk-return trade-off for international (France, Germany, Netherlands, Spain, UK, and US) government bond markets and the US stock market. We measure risk by the higher order moments (volatility, skewness, and excess kurtosis) as they are defined in

| [1] |

Aslanidis N, Christiansen C, Savva CS (2021) Quantile Risk-Return Trade-Off. J Risk Financ Manage 14: 249. https://doi.org/10.3390/jrfm14060249 doi: 10.3390/jrfm14060249

|

| [2] |

Atilgan Y, Bali TG, Demirtas KO, et al. (2020) Left-tail Momentum: Underreaction to Bad News, Costly Arbitrage and Equity Returns. J Financ Econ 135: 725–753. https://doi.org/10.1016/j.jfineco.2019.07.006 doi: 10.1016/j.jfineco.2019.07.006

|

| [3] |

Bai J, Bali TG, Wen Q (2021) Is there a Risk-Return Tradeoff in the Corporate Bond Market? Time-Series and Cross-Sectional Evidence. J Financ Econ 142: 1017–1037. https://doi.org/10.1016/j.jfineco.2021.05.003 doi: 10.1016/j.jfineco.2021.05.003

|

| [4] |

Delis M, Savva CS, Theodossiou P (2021) The Impact of the Coronavirus Crisis on the Market Price of Risk. J Financ Stabil 53: 100840. https://doi.org/10.1016/j.jfs.2020.100840 doi: 10.1016/j.jfs.2020.100840

|

| [5] |

Feunou B, Jahan-Parvar MR, Okou C (2018) Downside Variance Risk Premium. J Financ Econometrics 16: 341–383. https://doi.org/10.1016/j.jfs.2020.100840 doi: 10.1016/j.jfs.2020.100840

|

| [6] |

Feunou B, Jahan-Parvar MR, Tédongap R (2013) Modeling Market Downside Volatility. Rev Financ 17: 443–481. https://doi.org/10.1093/rof/rfr024 doi: 10.1093/rof/rfr024

|

| [7] |

Ghysels E, Santa-Clara P, Valkanov R (2005) There is a Risk-Return Tradeoff After All. J Financ Econ 76: 509–548. https://doi.org/10.1016/j.jfineco.2004.03.008 doi: 10.1016/j.jfineco.2004.03.008

|

| [8] |

Glosten LR, Jagannathan R, Runkle DE (1993) On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. J Financ 48: 1779–1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x doi: 10.1111/j.1540-6261.1993.tb05128.x

|

| [9] |

Kilic M, Shaliastovic I (2018) Good and Bad Variance Premia and Expected Returns. Manage Sci 65: 2522–2544. https://doi.org/10.1287/mnsc.2017.2890 doi: 10.1287/mnsc.2017.2890

|

| [10] |

Newey WK, West KD (1987) A Simple, Positive Semi-definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. Econometrica 55: 703–708. https://doi.org/10.2307/1913610 doi: 10.2307/1913610

|

| [11] |

Merton RC (1973) An Intertemporal Capital Asset Pricing Model. Econometrica 41: 867–887. https://doi.org/10.2307/1913811 doi: 10.2307/1913811

|

| [12] |

Savva CS, Theodossiou P (2018) The Risk and Return Conundrum Explained: International Evidence. J Financ Econometrics 16: 486–521. https://doi.org/10.1093/jjfinec/nby014 doi: 10.1093/jjfinec/nby014

|

| [13] |

Zhang Y, Ma F, Liang C, et al. (2021) Good Variance, Bad Variance, and Stock Return Predictability. Int J Financ Econ 26: 4410–4423. https://doi.org/10.1002/ijfe.2022 doi: 10.1002/ijfe.2022

|

QFE-07-02-013-s001.pdf QFE-07-02-013-s001.pdf |

|

Figures(1) / Tables(5)

Charlotte Christiansen, Christos S. Savva. Government bond market risk-return trade-off[J]. Quantitative Finance and Economics, 2023, 7(2): 249-260. doi: 10.3934/QFE.2023013

DownLoad:

DownLoad: