Citation: Joanna Olbrys, Elzbieta Majewska. Asymmetry Effects in Volatility on the Major European Stock Markets: the EGARCH Based Approach[J]. Quantitative Finance and Economics, 2017, 1(4): 411-427. doi: 10.3934/QFE.2017.4.411

| [1] | Abbas Q, Khan S, Shah SZA (2013) Volatility Transmission in Regional Asian Stock Markets. Emerg Mark Rev 16: 66–77. |

| [2] | Adkins LC (2014) Using Gretl for Principles of Econometrics, 4th Edition, Version 1.041. |

| [3] | Balaban E, Bayar A (2005) Stock Returns and Volatility: Empirical Evidence from Fourteen Countries. App Econ Lett 12: 603–611. |

| [4] | Baillie RT, Bollerslev T (1990) A Multivariate Generalized ARCH Approach to Modeling Risk Premia in Forward Foreign Exchange Rate Markets. J Int Money Financ 9: 309–324. |

| [5] | Baumöhl E, Výrost T (2010) Stock Market Integration: Granger Causality Testing with Respect to Nonsynchronous Trading Effects. Financ Uver 60: 414–425. |

| [6] | Bauwens L, Laurent S, Rombouts JVK (2006) Multivariate GARCH Models: A Survey. J App Econom 21: 79–109. |

| [7] | Bhar R (2001) Return and Volatility Dynamics in the Spot and Futures Markets in Australia: an Intervention Analysis in a Bivariate EGARCH-X Framework. J Futures Markets 21: 833–850. |

| [8] | Bhar R, Nikolova B (2009) Return, Volatility Spillovers and Dynamic Correlation in the BRIC Equity Markets: An Analysis Using a Bivariate EGARCH Framework. Glob Financ J 19: 203–218. |

| [9] | Black F (1976) Studies of Stock Market Volatility Changes. 1976 Proc Am Stat Assoc, Bus Econ Stat Section: 177–181. |

| [10] | Bollerslev T, Mikkelsen HO (1996) Modeling and Pricing Long Memory in Stock Market Volatility. J Econom 73: 151–184. |

| [11] | Bollerslev T, Wooldridge JM (1992) Quasi-Maximum Likelihood Estimation and Inference in Dynamic Models with Time-Varying Covariances. Econom Rev 11: 143–179. |

| [12] | Booth GG, Martikainen T, Tse Y (1997) Price and Volatility Spillovers in Scandinavian Stock Markets. J Bank Financ 21: 811–823. |

| [13] | Braun PA, Nelson DB, Sunier AM (1995) Good News, Bad News, Volatility, and Betas. J Financ 50: 1575–1603. |

| [14] | Bry G, Boschan C (1971) Cyclical Analysis of Time Series: Selected Procedures and Computer Programs, NBER: New York. |

| [15] | Campbell JY, Lo AW, MacKinlay AC (1997) The Econometrics of Financial Markets, Princeton University Press, New Jersey. |

| [16] | Curto JD, Tomaz JA, Pinto JC (2009) A New Approach to Bad News Effects on Volatility: The Multiple-Sign-Volume Sensitive Regime EGARCH Model (MSV-EGARCH). Port Econ J 8: 23–36. |

| [17] | Dedi L, Yavas BF (2016) Return and Volatility Spillovers in Equity Markets: An Investigation Using Various GARCH Methodologies. Cogent Econ Financ 4: 1–18. |

| [18] | Doornik JA, Hansen H (2008) An Omnibus Test for Univariate and Multivariate Normality. Oxford B Econ Stat 70: 927–939. |

| [19] | Engle RF (ed.) (2000) ARCH. Selected Readings, Oxford University Press. |

| [20] |

Engle RF, Ng VK (1993) Measuring end Testing the Impact of News on Volatility. J Financ 48: 1749–1778. doi: 10.1111/j.1540-6261.1993.tb05127.x

|

| [21] | Eun CS, Shim S (1989) International Transmission of Stock Market Movements. J Financ Quant Anal 24: 241–256. |

| [22] | Fabozzi FJ, Francis JC (1977) Stability Tests for Alphas and Betas over Bull and Bear Market Conditions. J Financ 32: 1093–1099. |

| [23] | Jane TD, Ding CG (2009) On the Multivariate EGARCH Model. Appl Econ Lett 16: 1757–1761. |

| [24] | Koutmos G, Booth GG (1995) Asymmetric Volatility Transmission in International Stock Markets. J Int Money Financ 14: 747–762. |

| [25] | Kuttu S (2014) Return and Volatility Dynamics Among Four African Equity Markets: A Multivariate VAR-EGARCH Analysis. Glob Financ J 25: 56–69. |

| [26] | Lee J, Stewart G (2010) Asymmetric Volatility and Volatility Spillovers in Baltic and Nordic Stock Markets. European J Econ, Financ Adm Sci 25: 136–143. |

| [27] | Lee JS, Kuo CT, Yen PH (2011) Market States and Initial Returns: Evidence from Taiwanese IPOs. Emerg Mark Financ Tr 47: 6–20. |

| [28] | Ljung G, Box GEP (1978) On a Measure of Lack of Fit in Time Series Models. Biometrika 66: 67–72. |

| [29] | Lucchetti K, Balietti S (2011) The gig package, Version 2.2. |

| [30] | Nelson DB (1991) Conditional Heteroskedasticity in Asset Returns: A New Approach. Econom 59: 347–370. |

| [31] | Olbrys J (2013a) Price and Volatility Spillovers in the Case of Stock Markets Located in Different Time Zones. Emerg Mark Financ Tr 49: 145–157. |

| [32] | Olbryś J (2013b) Asymmetric Impact of Innovations on Volatility in the Case of the US and CEEC-3 Markets: EGARCH Based Approach. Dynamic Econom Models 13: 33–50. |

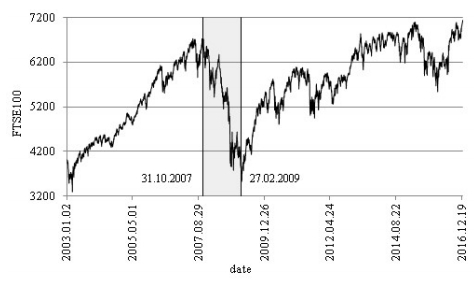

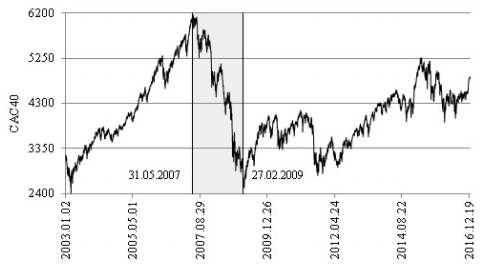

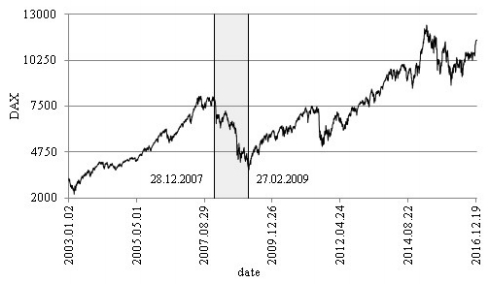

| [33] | Olbrys J, Majewska E (2014a) Quantitative Identification of Crisis Periods on the Major European Stock Markets. Pensee J 76: 254–260. |

| [34] | Olbrys J, Majewska E (2014b) On Some Empirical Problems in Financial Databases. Pensee J 76: 2–9. |

| [35] |

Olbryś J, Majewska E (2015) Bear Market Periods During the 2007–2009 Financial Crisis: Direct Evidence from the Visegrad Countries. Acta Oecon 65: 547–565. doi: 10.1556/032.65.2015.4.3

|

| [36] | Pagan AR, Sossounov KA (2003) A Simple Framework for Analysing Bull and Bear Markets. Appl Econ 18: 23–46. |

| [37] | Reyes MG (2001) Asymmetric Volatility Spillover in the Tokyo Stock Exchange. J Econ Financ 25: 206–213. |

| [38] | Scheicher M (2001) The Comovements of Stock Markets in Hungary, Poland and the Czech Republic. Int J Financ Econ 6: 27–39. |

| [39] | Tsay RS (2010) Analysis of Financial Time Series, John Wiley, New York. |

| [40] | Tse Y, Wu C, Young A (2003) Asymmetric Information Transmission between a Transition Economy and the U.S. Market: Evidence from the Warsaw Stock Exchange. Glob Financ J 14: 319–332. |

| [41] | Yang SY, Doong SC (2004) Price and Vilatility Spillovers between Stock Prices and Exchange Rates: Empirical Evidence from the G-7 Countries. Int J Bus Econ 3: 139–153. |

Figures(3) / Tables(5)

Joanna Olbrys, Elzbieta Majewska. Asymmetry Effects in Volatility on the Major European Stock Markets: the EGARCH Based Approach[J]. Quantitative Finance and Economics, 2017, 1(4): 411-427. doi: 10.3934/QFE.2017.4.411

DownLoad:

DownLoad: