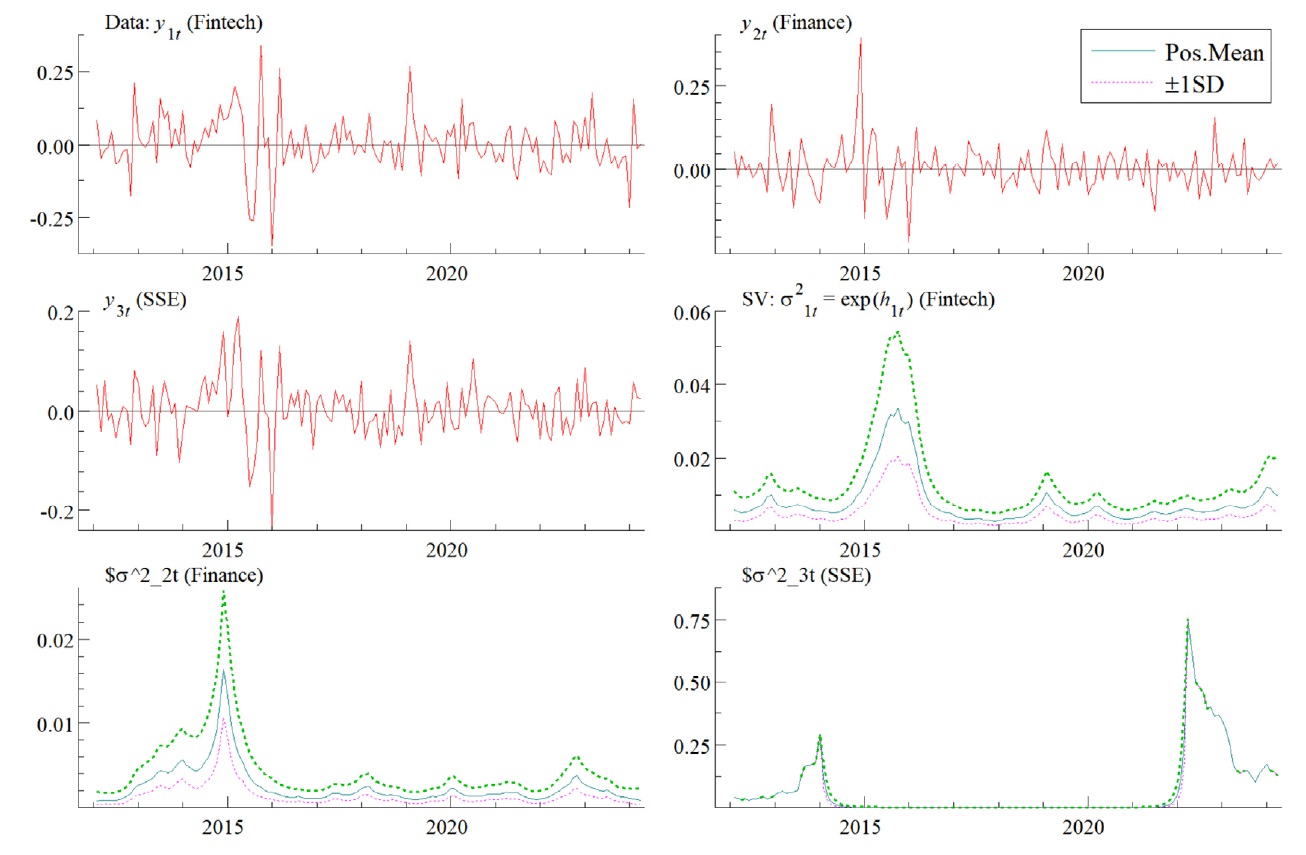

This paper examined the dynamic relationship between FinTech development and financial development using the time-varying parameter structural vector autoregression (TVP-SV-VAR) model to analyze their impulse response relationship. The results showed that the impact of FinTech development on financial development varies across different periods. In China, before the first half of 2021, financial development mainly drove FinTech development through demand. Afterward, FinTech development promoted financial development by providing new technological tools and services. In the United States, FinTech innovation and application mainly influenced financial development through supply-driven mechanisms. After the second half of 2022, as FinTech infrastructure improved, its positive impact on the financial market strengthened. The study also found that the effects of policy changes and market fluctuations on impulse responses at specific time points differed even in countries with different systems. The findings of this paper provide valuable insights for policymakers to address the challenges and opportunities brought on by FinTech.

Citation: Zekai Tu, Runze Yang, Cunyi Yang. Dynamics between FinTech and financial market: Supply-driven or Demand-guided?[J]. Quantitative Finance and Economics, 2024, 8(4): 658-677. doi: 10.3934/QFE.2024025

This paper examined the dynamic relationship between FinTech development and financial development using the time-varying parameter structural vector autoregression (TVP-SV-VAR) model to analyze their impulse response relationship. The results showed that the impact of FinTech development on financial development varies across different periods. In China, before the first half of 2021, financial development mainly drove FinTech development through demand. Afterward, FinTech development promoted financial development by providing new technological tools and services. In the United States, FinTech innovation and application mainly influenced financial development through supply-driven mechanisms. After the second half of 2022, as FinTech infrastructure improved, its positive impact on the financial market strengthened. The study also found that the effects of policy changes and market fluctuations on impulse responses at specific time points differed even in countries with different systems. The findings of this paper provide valuable insights for policymakers to address the challenges and opportunities brought on by FinTech.

| [1] |

Alyakoob M, Rahman MS, Wei Z (2021) Where You Live Matters: Local Bank Competition, Online Marketplace Lending, and Disparity in Borrower Benefits. Inform Syst Res 32: 1390–1411. https://doi.org/10.1287/ISRE.2021.1043 doi: 10.1287/ISRE.2021.1043

|

| [2] |

Anagnostopoulos I (2018) Fintech and regtech: Impact on regulators and banks. J Econ Bus 100: 7–25. https://doi.org/10.1016/j.jeconbus.2018.07.003 doi: 10.1016/j.jeconbus.2018.07.003

|

| [3] |

Benoit S, Colliard JE, Hurlin C, et al. (2017) Where the risks lie: A survey on systemic risk. Rev Financ 21: 109–152. https://doi.org/10.1093/rof/rfw026 doi: 10.1093/rof/rfw026

|

| [4] |

Berg T, Fuster A, Puri M (2022) FinTech lending. Annu Rev Financ Econ 14: 187–207. https://doi.org/10.1146/annurev-financial-101521-112042 doi: 10.1146/annurev-financial-101521-112042

|

| [5] |

Bollaert H, Lopez-de-Silanes F, Schwienbacher A (2021) Fintech and access to finance. J Corp Financ 68: 101941. https://doi.org/10.1016/j.jcorpfin.2021.101941 doi: 10.1016/j.jcorpfin.2021.101941

|

| [6] |

Boot A, Hoffmann P, Laeven L, et al. (2021) Fintech: what's old, what's new? J Financ Stabil 53: 100836. https://doi.org/10.1016/j.jfs.2020.100836 doi: 10.1016/j.jfs.2020.100836

|

| [7] |

Buchak G, Matvos G, Piskorski T, et al. (2018) Fintech, regulatory arbitrage, and the rise of shadow banks. J Financ Econ 130: 453–483. https://doi.org/10.1016/j.jfineco.2018.03.011 doi: 10.1016/j.jfineco.2018.03.011

|

| [8] |

Chaklader B, Gupta BB, Panigrahi PK (2023) Analyzing the progress of FINTECH-companies and their integration with new technologies for innovation and entrepreneurship. J Bus Res 161: 113847. https://doi.org/10.1016/j.jbusres.2023.113847 doi: 10.1016/j.jbusres.2023.113847

|

| [9] | Christensen CM (2013) The innovator's dilemma: when new technologies cause great firms to fail, Harvard Business Review Press. |

| [10] |

Cogley T, Sargent TJ (2001) Evolving Post-World War Ⅱ U.S. Inflation Dynamics. NBER Macroecon Annu 16: 331–373. https://doi.org/10.1086/654451 doi: 10.1086/654451

|

| [11] |

Di Maggio M, Yao V (2021) Fintech Borrowers: Lax Screening or Cream-Skimming? Rev Financ Stud 34: 4565–4618. https://doi.org/10.1093/rfs/hhaa142 doi: 10.1093/rfs/hhaa142

|

| [12] |

Ding N, Gu L, Peng Y (2022) Fintech, financial constraints and innovation: Evidence from China. J Corp Financ 73: 102194. https://doi.org/10.1016/j.jcorpfin.2022.102194 doi: 10.1016/j.jcorpfin.2022.102194

|

| [13] |

Drasch BJ, Schweizer A, Urbach N (2018) Integrating the 'Troublemakers': A taxonomy for cooperation between banks and fintechs. J Econ Bus 100: 26–42. https://doi.org/10.1016/j.jeconbus.2018.04.002 doi: 10.1016/j.jeconbus.2018.04.002

|

| [14] |

Erel I, Liebersohn J (2022) Can FinTech reduce disparities in access to finance? Evidence from the Paycheck Protection Program. J Financ Econ 146: 90–118. https://doi.org/10.1016/j.jfineco.2022.05.004 doi: 10.1016/j.jfineco.2022.05.004

|

| [15] |

Fu J, Mishra M (2022) Fintech in the time of COVID− 19: Technological adoption during crises. J Financ Intermed 50: 100945. https://doi.org/10.1016/j.jfi.2021.100945 doi: 10.1016/j.jfi.2021.100945

|

| [16] |

Gomber P, Koch JA, Siering M (2017) Digital Finance and FinTech: current research and future research directions. J Bus Econ 87: 537–580. https://doi.org/10.1007/s11573-017-0852-x doi: 10.1007/s11573-017-0852-x

|

| [17] |

Gopal M, Schnabl P (2022) The rise of finance companies and fintech lenders in small business lending. Rev Financ Stud 35: 4859–4901. https://doi.org/10.1093/rfs/hhac034 doi: 10.1093/rfs/hhac034

|

| [18] |

Hendershott T, Zhang X, Zhao JL, et al. (2021) FinTech as a game changer: Overview of research frontiers. Inform Syst Res 32: 1–17. https://doi.org/10.1287/isre.2021.0997 doi: 10.1287/isre.2021.0997

|

| [19] |

Hirsch-Kreinsen H (2011) Financial Market and Technological Innovation. Ind Innov 18: 351–368. https://doi.org/10.1080/13662716.2011.573954 doi: 10.1080/13662716.2011.573954

|

| [20] |

Kommel KA, Sillasoo M, Lublóy Á (2019) Could crowdsourced financial analysis replace the equity research by investment banks? Financ Res Lett 29: 280–284. https://doi.org/10.1016/j.frl.2018.08.007 doi: 10.1016/j.frl.2018.08.007

|

| [21] |

Lagna A, Ravishankar MN (2022) Making the world a better place with fintech research. Inform Syst J 32: 61–102. https://doi.org/10.1111/isj.12333 doi: 10.1111/isj.12333

|

| [22] |

Lee I, Shin YJ (2018) Fintech: Ecosystem, business models, investment decisions, and challenges. Bus Horizons 61: 35–46. https://doi.org/10.1016/j.bushor.2017.09.003 doi: 10.1016/j.bushor.2017.09.003

|

| [23] |

Li J, Li J, Zhu X, et al. (2020) Risk spillovers between FinTech and traditional financial institutions: Evidence from the U.S. Int Rev Financ Anal 71: 101544. https://doi.org/10.1016/j.irfa.2020.101544 doi: 10.1016/j.irfa.2020.101544

|

| [24] |

Lovreta L, López Pascual J (2020) Structural breaks in the interaction between bank and sovereign default risk. SERIEs 11: 531–559. https://doi.org/10.1007/s13209-020-00219-z doi: 10.1007/s13209-020-00219-z

|

| [25] |

Moro-Visconti R, Cruz Rambaud S, López Pascual J (2023) Artificial intelligence-driven scalability and its impact on the sustainability and valuation of traditional firms. Hum Soc Sci Commun 10: 795. https://doi.org/10.1057/s41599-023-02214-8 doi: 10.1057/s41599-023-02214-8

|

| [26] |

Muganyi T, Yan L, Yin Y, et al. (2022) Fintech, regtech, and financial development: evidence from China. Financial Innovation 8: 29. https://doi.org/10.1186/s40854-021-00313-6 doi: 10.1186/s40854-021-00313-6

|

| [27] | Nakajima J (2011) Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Monetary Econ Stud 29: 107–142. |

| [28] |

Parlour CA, Rajan U, Zhu H (2022) When fintech competes for payment flows. Rev Financ Stud 35: 4985–5024. https://doi.org/10.1093/rfs/hhac022 doi: 10.1093/rfs/hhac022

|

| [29] |

Primiceri GE (2005) Time Varying Structural Vector Autoregressions and Monetary Policy. Rev Econ Stud 72: 821–852. https://doi.org/10.1111/j.1467-937X.2005.00353.x doi: 10.1111/j.1467-937X.2005.00353.x

|

| [30] |

Roh T, Yang YS, Xiao S, et al. (2024) What makes consumers trust and adopt fintech? An empirical investigation in China. Electron Commer Res 24, 3–35. https://doi.org/10.1007/s10660-021-09527-3 doi: 10.1007/s10660-021-09527-3

|

| [31] |

Saklain MS (2024) FinTech, systemic risk and bank market power – Australian perspective. Int Rev Financ Anal 95: 103351. https://doi.org/10.1016/j.irfa.2024.103351 doi: 10.1016/j.irfa.2024.103351

|

| [32] | Tao R, Su CW, Naqvi B, et al. (2022) Can Fintech development pave the way for a transition towards low-carbon economy: A global perspective. Technol Forecast Soc 174: 121278. |

| [33] |

Thakor AV (2020) Fintech and banking: What do we know? J Financ Intermed 41: 100833. https://doi.org/10.1016/j.jfi.2019.100833 doi: 10.1016/j.jfi.2019.100833

|

| [34] |

Wen S, Li J, Huang C, et al. (2023) Extreme risk spillovers among traditional financial and FinTech institutions: A complex network perspective. Q Rev Econ Financ 88: 190–202. https://doi.org/10.1016/j.qref.2023.01.005 doi: 10.1016/j.qref.2023.01.005

|

| [35] |

Yao M, Di H, Zheng X, et al. (2018) Impact of payment technology innovations on the traditional financial industry: A focus on China. Technol Forecast Soc 135: 199–207. https://doi.org/10.1016/j.techfore.2017.12.023 doi: 10.1016/j.techfore.2017.12.023

|

Figures(12) / Tables(2)

Zekai Tu, Runze Yang, Cunyi Yang. Dynamics between FinTech and financial market: Supply-driven or Demand-guided?[J]. Quantitative Finance and Economics, 2024, 8(4): 658-677. doi: 10.3934/QFE.2024025

DownLoad:

DownLoad: