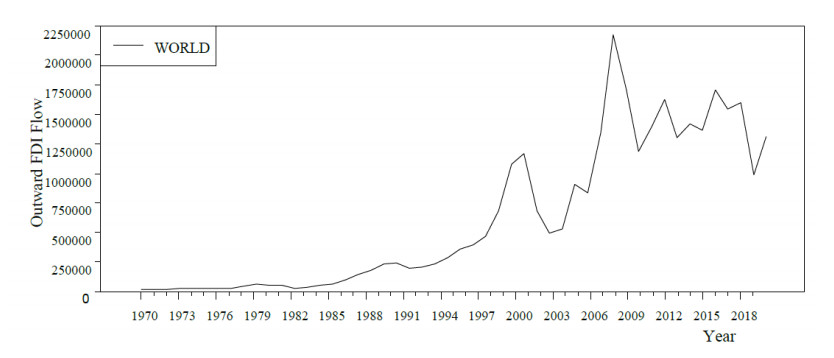

Over the past few decades, large numbers of literatures in behavior finance have examined firm's internationalization motives, with focused on how host country's risk components affect investment inflow. But the effects of home country risk on investment outflow remain unexamined. Therefore, based on the conceptualization of FDI escapism and the combine frameworks of Dunning's eclectic paradigm and internationalization theory, the objectives of this study are twofold: First, to examine and explain the effects of home country composite risks (which encompasses economic risks, financial risks, political risk) on firms' internationalization motive through outward FDI. Second, to determine which components of home country risk "pushes" firms to initiate the FDI escapism phenomenon in global market. Findings reveal that home country composite risk has moderate adverse effect on investment flow abroad, contributed by both the political and financial risk components, which may give rise to escaping FDI. These findings suggest that firm may initiate outward FDI as a partial escape strategy to address the political and financial challenges in their home country. These results are robust to endogeneity issue and have several substantial implications for policy design to reduce country risks in order to achieve firm's specific objective and government policy goals.

Citation: Osarumwense Osabuohien-Irabor, Igor M. Drapkin. FDI Escapism: the effect of home country risks on outbound investment in the global economy[J]. Quantitative Finance and Economics, 2022, 6(1): 113-137. doi: 10.3934/QFE.2022005

Over the past few decades, large numbers of literatures in behavior finance have examined firm's internationalization motives, with focused on how host country's risk components affect investment inflow. But the effects of home country risk on investment outflow remain unexamined. Therefore, based on the conceptualization of FDI escapism and the combine frameworks of Dunning's eclectic paradigm and internationalization theory, the objectives of this study are twofold: First, to examine and explain the effects of home country composite risks (which encompasses economic risks, financial risks, political risk) on firms' internationalization motive through outward FDI. Second, to determine which components of home country risk "pushes" firms to initiate the FDI escapism phenomenon in global market. Findings reveal that home country composite risk has moderate adverse effect on investment flow abroad, contributed by both the political and financial risk components, which may give rise to escaping FDI. These findings suggest that firm may initiate outward FDI as a partial escape strategy to address the political and financial challenges in their home country. These results are robust to endogeneity issue and have several substantial implications for policy design to reduce country risks in order to achieve firm's specific objective and government policy goals.

| [1] | Asgari M, Ahmad SZ, Gurrib I (2010) Explaining the Internationalization Process of Malaysian Service Firms. Int J Trade Econ Financ 1. https://ssrn.com/abstract = 2345640 |

| [2] |

Avioutskii V, Tensaout M (2016) Does politics matter? Partisan FDI in Central and Eastern Europe. Multinatl Bus Rev 24: 375–398. https://doi.org/10.1108/MBR-07-2015-0028 doi: 10.1108/MBR-07-2015-0028

|

| [3] |

Abdallah W, Goergen M, O'Sullivan N (2015) Endogeneity: How Failure to Correct for itcan Cause Wrong Inferences and Some Remedies. Br J Manage 26: 791–804. https://doi.org/10.1111/1467-8551.12113 doi: 10.1111/1467-8551.12113

|

| [4] |

Anderson E, Gatignon H (1986) Modes of Foreign Entry: A Transaction Cost Analysis and Propositions. J Int Bus Stud 17: 1–26. https://doi.org/10.1057/palgrave.jibs.8490432 doi: 10.1057/palgrave.jibs.8490432

|

| [5] |

Arellano M, Bond S (1991) Some tests of specification for panel data: Monte Carl evidence and an application to employment equations. Rev Econ Stud 58: 277–297. https://doi.org/10.2307/2297968 doi: 10.2307/2297968

|

| [6] | Aguiar S, Aguiar-Conraria L, Gulamhussen MA, et al. (2012) Foreign direct investment and home-country political risk: The case of Brazil. Latin Am Res Rev 47: 144–165. https://www.jstor.org/stable/23321736 |

| [7] |

Arellano M, Bover O (1995) Another look at the instrumental variable estimation of errorcomponents models. J Econ 68: 29–51. https://doi.org/10.1016/03044076 (94)01642-D doi: 10.1016/03044076(94)01642-D

|

| [8] | Buckley PJ, Voss H, Cross A, et al. (2011) The emergence of Chinese firms as multinationals: The influence of the home institutional environment, R.D. Pearce (Ed.), China and the multinationals: Edward Elgar Publishing. https://doi.org/10.4337/9781781001110.00012 |

| [9] | Buckley PJ, Casson MC (1976) The future of multinational enterprise, New York: Holmer and Meier Publishers. http://pi.lib.uchicago.edu/1001/cat/bib/211161 |

| [10] |

Barry CM, DiGiuseppe M (2019) Transparency, Risk, and FDI. Polit Res Q 72: 132–146. https://doi.org/10.1177/1065912918781037 doi: 10.1177/1065912918781037

|

| [11] |

Blundell R, Bond S (1998) Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. J Econometrics 87: 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8 doi: 10.1016/S0304-4076(98)00009-8

|

| [12] |

Bond SR (2002) Dynamic panel data models: a guide to micro data methods and practice. Port Econ J 1: 141–162. https://doi.org/10.1007/s10258-002-0009-9 doi: 10.1007/s10258-002-0009-9

|

| [13] |

Barnard H, Luiz JM (2018) Escape FDI and the dynamics of a cumulative process of institutional misalignment and contestation: Stress, strain and failure. J World Bus 53: 605–619. https://doi.org/10.1016/j.jwb.2018.03.010 doi: 10.1016/j.jwb.2018.03.010

|

| [14] | Boddewyn JJ (1988) Political Aspects of MNE Theory. J Int Bus Stud 19: 341–363. http://www.jstor.org/stable/155130 |

| [15] |

Brouthers LE, Mukhopadhyay S, Wilkinson T, et al. (2009) International Market Selection and Subsidiary Performance: A Neural Network Approach. J World Bus 44: 262–273. https://doi.org/10.1016/j.jwb.2008.08.004 doi: 10.1016/j.jwb.2008.08.004

|

| [16] |

Chen C (2015) Determinants and motives of outward foreign direct investment from China's provincial firms. Trans Corp 23: 1–28. https://doi.org/10.18356/6ba5ab37-en doi: 10.18356/6ba5ab37-en

|

| [17] |

Caves RE, Porter ME (1977) From entry barriers to mobility barriers: Conjectural decisions and contrived deterrence to new competition. Q J Econ 91: 241–261. https://doi.org/10.2307/1885416 doi: 10.2307/1885416

|

| [18] |

Cuervo-Cazurra A, Narula R, Un CA (2015) Internationalization motives: sell more, buy better, upgrade and escape. Multinatl Bus Rev 23: 25–35. https://doi.org/10.1108/MBR-02-2015-0009 doi: 10.1108/MBR-02-2015-0009

|

| [19] | Cuervo-Cazurra A, Ramamurti R (2015) The escape motivation of emerging market multinational enterprises, Columbia University Libraries. https://doi/10.7916/D86H4GJJ |

| [20] |

Cantwell J, Narula R (2001) The eclectic paradigm in the global economy. Int J Econ Bus 8: 155–172. https://doi.org/10.1080/13571510110051504 doi: 10.1080/13571510110051504

|

| [21] |

Doh J, Rodrigues S, Saka-Helmhout A (2017) International bus. responses to institutional voids. J Int Bus Stud 48: 293–307. https://doi.org/10.1057/s41267-017-0074-z doi: 10.1057/s41267-017-0074-z

|

| [22] | Domke-Damonte D (2000) Interactive effects of international strategy and throughput technology on entry mode for service firms. Manage Int Rev 40: 41–59. https://www.jstor.org/stable/40835866 |

| [23] | Dunning JH (1977) Trade, location of economic activity and the MNE: A search for an eclectic approach, In: B. Ohlin, P. O. Hesselborn & P. M. Wijkman (Eds.), The international allocation of economic activity, Macmillan, 395–418. https://doi.org/10.1007/978-1-349-03196-2_38 |

| [24] | Dunning JH, Lundan SM (2008) Multinational Enterprises and the Global Economy, Edward, Elgar Publishing Limited, Cheltenham, 79–115. https://dipiufabc.files.wordpress.com |

| [25] |

Dunning JH, Lundan SM (2008) Institutions and the OLI paradigm of the multinational enterprise. Asia Pac J Manage 25: 573–593. https://doi.org/10.1007/s10490-007-9074-z doi: 10.1007/s10490-007-9074-z

|

| [26] | David U (2021) Global fall in foreign investment reflects rise in geopolitical tensions, Australia strategy and policy institute. Available from: https://www.aspistrategist.org.au/global-fall-in-foreign investment-reflects-rise-in-geopolitical-tensions/. |

| [27] | Dunning JH (1981) Int production and the multinational enterprise, London: Allen & Unwin. |

| [28] |

Dunning JH, Robson P (1987) Multinational corporate integration and regional economic integration. J Common Mark Stud 26: 103–125. https://doi.org/10.1080/03050627408434383 doi: 10.1080/03050627408434383

|

| [29] | Dunning JH (1993a) The globalisation of business, London, https://doi.org/10.4324/9781315743691 |

| [30] | Dunning JH (1993b) Mult enterprises and the global economy, Wokingham: Addision Wesley. |

| [31] |

Enderwick P (2017) Viewpoint escape FDI from emerging markets: clarifying and extending the concept. Int J Emerg Mark 12: 418–426. https://doi.org/10.1108/IJoEM-11-2016-0325 doi: 10.1108/IJoEM-11-2016-0325

|

| [32] |

GaoYan Q (2020) Political risk distribution of Chinese outward foreign direct investment. Int J Emerg Mark 16: 1202–1227. https://doi.org/10.1108/IJOEM-06-2018-0344 doi: 10.1108/IJOEM-06-2018-0344

|

| [33] |

Gammeltoft P, Pradhan JP, Goldstein A (2010) Emerging multinationals: Home and host country determinants and outcomes. Int J Emerg Mark 5: 254–265. https://doi.org/10.1108/17468801011058370 doi: 10.1108/17468801011058370

|

| [34] | Greene WH (2012) Econometric Analysis, Prentice Hall, Upper Saddle River. Available from: https://spu.fem.uniag.sk |

| [35] |

García-Canal E, Guillén MF (2008) Risk and the Strategy of Foreign Location Choice in Regulated Industries. Strat Manage J 29: 1097–1115. http://dx.doi.org/10.1002/smj.692 doi: 10.1002/smj.692

|

| [36] | Håkansson H (1987) Industrial tech development: A network approach, London: Croom Helm. https://doi.org/10.1016/0737-6782(87)90076-2 |

| [37] |

Hoque ME, Akhter T, Yakob NA (2018) Revisiting endogeneity among foreign direct investment, economic growth and stock market development: Moderating role of political instability. Cogent Econ Financ 6. http://doi.org/10.1080/23322039.2018.1492311 doi: 10.1080/23322039.2018.1492311

|

| [38] |

Huang HH, Chan ML, Chang YS (2010) Risk to firm value for Taiwanese companies investing in china: Who fares better? Rev Pacific Basin Financ Mark Policies 13: 237–266. http://doi.org/10.1142/S0219091510001937 doi: 10.1142/S0219091510001937

|

| [39] |

Henisz WJ, Zelner BA (2003) The strategic organization of political risks and opportunities. Strat Organ 1: 451–460. http://doi.org/10.1177/14761270030014005 doi: 10.1177/14761270030014005

|

| [40] | Holburn GLF, Zelner BA (2010) Political Capabilities, Policy Risk, and International Investment Strategy: Evidence from the Global Electric Power Generation Industry. Strat Manage J 31: 1290–1315. https://www.jstor.org/stable/40927699 |

| [41] |

Hansen LP (1982) Large Sample Properties of Generalized Method of Moments Estimators. Econometrica 50: 1029–1054. https://doi.org/10.2307/1912775 doi: 10.2307/1912775

|

| [42] | Hymer SH (1960) The int. operations of national firms: A study of direct foreign investment. Unpublished PhD Dissertation, Massachusetts Institute of Technology, Cambridge, MA. |

| [43] |

Johanson J, Wiedersheim-Paul F (1975) The internationalization of the firm. J Manage Stud 12: 305–322. https://doi.org/10.1111/j.1467-6486.1975.tb00514.x doi: 10.1111/j.1467-6486.1975.tb00514.x

|

| [44] |

Jiménez A (2010) Does political risk affect the scope of the expansion abroad? Evidence from Spanish MNEs. Int Bus Rev 19: 619–633. http://doi.org/10.1016/j.ibusrev.2010.03.004 doi: 10.1016/j.ibusrev.2010.03.004

|

| [45] |

Jiménez A, Luis-Rico I, Benito-Osorio D (2014) The influence of political risk on the scope of internationalization of regulated companies: Insights from a Spanish sample. J World Bus 49: 301–311. https://doi.org/10.1016/j.jwb.2013.06.001 doi: 10.1016/j.jwb.2013.06.001

|

| [46] |

Kobrak C, Oesterle MJ, Rö ber B (2018) Escape FDI and the Varieties of Capitalism: Why History Matters in International Business. Manage Int Rev 58: 449–464. https://doi.org/10.1007/s11575-017-0323-1 doi: 10.1007/s11575-017-0323-1

|

| [47] | Khanna T, Palepu K (2010) Winning in emerging markets: A roadmap for strategy and execution, Boston, Massachusetts: Harvard Business Press. http://doi.org/10.1177/0974173920100316 |

| [48] |

Kamal MA, Ullah A, Zheng J, et al. (2019) Natural resource or market seeking motive of China's FDI in Asia? New evidence at income and sub-regional level. Econ Res Ekonomska Istraživanja 32: 3869–3894. https://doi.org/10.1080/1331677X.2019.1674679 doi: 10.1080/1331677X.2019.1674679

|

| [49] |

Kottaridi C, Giakoulas D, Manolopoulos D (2019) Escapism FDI from developed economies: The role of regulatory context and corporate taxation. Int Bus Rev 28: 36–47. https://doi.org/10.1016/j.ibusrev.2018.06.004. doi: 10.1016/j.ibusrev.2018.06.004

|

| [50] |

Latif Z, Jianqiu Z, Salam S, et al. (2017) FDI and political violence in Pakistan telecommunications. Human Syst Manage 36: 341–352. http://doi.org/10.3233/HSM-17154 doi: 10.3233/HSM-17154

|

| [51] |

Liang X, Lu X, Wang L (2012) Outward internationalisation of private enterprises in China: The effect of competitive advantages and disadvantage compared to home market rivals. J World Bus 47: 134–144. https://doi.org/10.1016/j.jwb.2011.02.002 doi: 10.1016/j.jwb.2011.02.002

|

| [52] | Liu H, Wang Y, Huang L, et al. (2021) Outward FDI and stock price crash risk Evidence from China. J Int Financ Mark Inst Money 73: 101366. https://doi.org/10.1016/j.intfin.2021.101366 |

| [53] |

Lu J, Huang X, Muchiri M (2017) Political Risk and Chinese Outward Foreign Direct Investment to Africa: The Role of Foreign Aid. Afr J Manage 3: 82–98. https://doi.org/10.1080/23322373.2016.1275941 doi: 10.1080/23322373.2016.1275941

|

| [54] | Michael AW, Lewin AY (2007) Outward Foreign Direct Investment as Escape Response to Home Country Institutional Constraints. J Int Bus Stud 38: 579–594. http://www.jstor.org/stable/4540444 |

| [55] |

Mehmet HT, Ö zlem SG (2016) The Effect of Country Risk on Foreign Direct Investment: A Dynamic Panel Data Analysis for Developing Countries. J Econ Library 3. http://dx.doi.org/10.1453/jel.v3i1.771 doi: 10.1453/jel.v3i1.771

|

| [56] | Mussa M (2000) Factors Driving Global Economic Integration. IMF. https://www.imf.org/en/News/Articles/2015/09/28/04/53/sp082500 |

| [57] | Neter J, Wasserman W, Kutner M (1985) Regression, analysis of variance and experimental designs, Applied linear statistical models, Homewood, IL: Richard D. Irwin. Inc. |

| [58] |

Nickel S (1981) Biases in Dynamic Models with Fixed Effects. Econometrica 49: 14171426. https://doi.org/10.2307/1911408 doi: 10.2307/1911408

|

| [59] |

Osabutey ELC, Okoro C (2015) Political Risk and Foreign Direct Investment in Africa: The Case of the Nigerian Telecommunications Industry. Thunderbird Int Bus Rev 57: 417–429. https://doi.org/10.1002/tie.21672 doi: 10.1002/tie.21672

|

| [60] |

Roodman D (2009) A note on the theme of too many instruments. Ox Bull Econ Stat 71: 135–158. https://doi.org/10.1111/j.1468-0084.2008.00542.x doi: 10.1111/j.1468-0084.2008.00542.x

|

| [61] |

Quer D, Claver E, Rienda L (2012) Political risk, cultural distance, and outward foreign direct investment: Empirical evidence from large Chinese firms. Asia Pac J Manage 29: 1089–1104. https://doi.org/10.1007/s10490-011-9247-7 doi: 10.1007/s10490-011-9247-7

|

| [62] | Rugman AM (1981) Inside the multinationals, New York: Columbia University Press. https://doi.org/10.2307/3114400 |

| [63] |

Sharma VM, Erramilli MK (2004) Resource-based explanation of entry mode choice. J Mark Theory Pract 12: 1–18. https://doi.org/10.1080/10696679.2004.11658509 doi: 10.1080/10696679.2004.11658509

|

| [64] |

Slangen AHL, van Tulder RJM (2009) Cultural distance, political risk, or governance quality? Towards a more accurate conceptualization and measurement of external uncertainty in foreign entry mode research. Int Bus Rev 18: 276–291. https://doi.org/10.1016/j.ibusrev.2009.02.014 doi: 10.1016/j.ibusrev.2009.02.014

|

| [65] |

Stoian C, Mohr A (2016) Outward foreign direct investment from emerging economies: escaping home country regulative voids. Int Bus Rev 25: 1124–1135. https://doi.org/10.1016/j.ibusrev.2016.02.004. doi: 10.1016/j.ibusrev.2016.02.004

|

| [66] |

Stoian C, Filippaios F (2008) Dunning's eclectic paradigm: A holistic, yet context specific framework for analysing the determinants of outward FDI: Evidence from international Greek investments. Int Bus Rev 17: 349–367. https://doi.org/10.1016/j.ibusrev.2007.12.005 doi: 10.1016/j.ibusrev.2007.12.005

|

| [67] |

Shao X (2020) Chinese ODI responses to the B & R initiative: Evidence from a quasi-natural experiment. China Econ Rev 61: 101435. https://doi.org/10.1016/j.chieco.2020. doi: 10.1016/j.chieco.2020

|

| [68] |

Stal E, Cuervo-Cazurra A (2011) The Investment Development Path and FDI From Developing Countries: The Role of Pro-Market Reforms and Institutional Voids. Latin Am Bus Rev 12: 209–231. https://doi.org/10.1080/10978526.2011.614174 doi: 10.1080/10978526.2011.614174

|

| [69] |

Tang RW, Buckley PJ (2020) Host country risk and foreign ownership strategy: Meta analysis and theory on the moderating role of home country institutions. Int Bus Rev 29: 101666. https://doi.org/10.1016/j.ibusrev.2020.101666. doi: 10.1016/j.ibusrev.2020.101666

|

| [70] | Tallman SB (1988) Home country political risk and foreign direct investment in the United States. J Int Bus Stud 19: 219–234. |

| [71] |

Vernon R (1966) International investment & international trade in the product cycle. Q J Econ 80: 190–207. https://doi.org/10.2307/1880689 doi: 10.2307/1880689

|

| [72] | Wooldridge JM (2010) Econometric Analysis of Cross Section and Panel Data, 2nd Edition, MIT Press, Cambridge. https://mitpress.mit.edu/books/ |

| [73] |

Wang C, Piperopoulos P, Chen S, et al. (2022) Outward FDI and Innovation Performance of Chinese Firms: Why can Home-grown political Ties be a Liability? J World Bus 57: 101306. https://doi.org/10.1016/j.jwb.2021.101306 doi: 10.1016/j.jwb.2021.101306

|

| [74] | Wang EZ, Lee CC (2021) Foreign direct investment, income inequality and country risk. Int J Financ Econ.[In press]. https://doi.org/10.1002/ijfe.2542 |

| [75] |

Wu J, Chen X (2014) Home country institutional environments and foreign expansion of emerging market firms. Int Bus Rev 23: 872. https://doi.org/10.1016/j.ibusrev.2014.01.004 doi: 10.1016/j.ibusrev.2014.01.004

|

| [76] |

Witt M, Lewin A (2007) Outward foreign direct investment as escape response to home country institutional constraints. J Int Bus Stud 38: 579–594. https://doi.org/10.1057/palgrave.jibs.8400285 doi: 10.1057/palgrave.jibs.8400285

|

| [77] | Whitelock J (2002) Theories of internationalisation and their impact on market entry. Int Mark Rev 19: 342–347. https://www.semanticscholar.org/paper/ |

| [78] |

Weng DH, Peng MW (2018) Home bitter home: How labour protection influences firm offshoring. J World Bus 53: 632–640. https://doi.org/10.1016/j.jwb.2018.03.007 doi: 10.1016/j.jwb.2018.03.007

|

QFE-06-01-005-s001.pdf QFE-06-01-005-s001.pdf |

|

Figures(2) / Tables(7)

Osarumwense Osabuohien-Irabor, Igor M. Drapkin. FDI Escapism: the effect of home country risks on outbound investment in the global economy[J]. Quantitative Finance and Economics, 2022, 6(1): 113-137. doi: 10.3934/QFE.2022005

DownLoad:

DownLoad: