Finance has an important influence on technological innovation (TI). There are several stages of, as well as various financial constraints on, TI. In this article, we divide TI into four stages: the development, growth, maturity, and decline stages. Concurrently, we classify TI funding sources into five types: enterprise funds, government funds, venture capital funds, loans from financial institutions, and capital market funds. Based on the analysis of the stages and financing constraints of TI, this paper constructs a state-space model to study the effects of various funding sources on TI in Hebei Province, China, from 2005 to 2018. The results show a long-term equilibrium relationship between finance and TI, whereby different financial methods have different effects on each stage of TI. Enterprise funds play a primary role in the development, growth, and maturity stages. Government funds play a prominent role in the development and growth stages. Capital market funds and loans from financial institutions only play a role in the maturity period. The role of capital market funds was positive, while that of loans from financial institutions was negative. The effect of venture capital was not noticeable at any stage. Finally, we give our conclusions and put forward some countermeasures and suggestions to promote TI in Hebei Province.

Citation: Mengxin Wang, Ran Gu, Meng Wang, Junru Zhang. Research on the impact of finance on promoting technological innovation based on the state-space model[J]. Green Finance, 2021, 3(2): 119-137. doi: 10.3934/GF.2021007

Related Papers:

[1]

Xinyu Fu, Yanting Xu .

The impact of digital technology on enterprise green innovation: quality or quantity?. Green Finance, 2024, 6(3): 484-517.

doi: 10.3934/GF.2024019

[2]

Tao Lin, Mingyue Du, Siyu Ren .

How do green bonds affect green technology innovation? Firm evidence from China. Green Finance, 2022, 4(4): 492-511.

doi: 10.3934/GF.2022024

[3]

Yanyan Yao, Dandan Hu, Cunyi Yang, Yong Tan .

The impact and mechanism of fintech on green total factor productivity. Green Finance, 2021, 3(2): 198-221.

doi: 10.3934/GF.2021011

[4]

Liudmila S. Kabir, Zhanna A. Mingaleva, Ivan D. Rakov .

Technological modernization of the national economy as an indicator of green finance: Data analysis on the example of Russia. Green Finance, 2025, 7(1): 146-174.

doi: 10.3934/GF.2025006

[5]

Pengzhen Liu, Yanmin Zhao, Jianing Zhu, Cunyi Yang .

Technological industry agglomeration, green innovation efficiency, and development quality of city cluster. Green Finance, 2022, 4(4): 411-435.

doi: 10.3934/GF.2022020

[6]

Yafei Wang, Jing Liu, Xiaoran Yang, Ming Shi, Rong Ran .

The mechanism of green finance's impact on enterprises' sustainable green innovation. Green Finance, 2023, 5(3): 452-478.

doi: 10.3934/GF.2023018

[7]

Mihaela Onofrei, Bogdan Narcis Fîrțescu, Florin Oprea, Dana Claudia Cojocaru .

The effects of environmental patents on renewable energy consumption. Green Finance, 2024, 6(4): 630-648.

doi: 10.3934/GF.2024024

[8]

Jun Duan, Tingting Liu, Xiaoran Yang, Hua Yang, Yunwei Gao .

Financial asset allocation and green innovation. Green Finance, 2023, 5(4): 512-537.

doi: 10.3934/GF.2023020

[9]

Reinhard Haas, Amela Ajanovic, Jasmine Ramsebner, Theresia Perger, Jaroslav Knápek, Jan W. Bleyl .

Financing the future infrastructure of sustainable energy systems. Green Finance, 2021, 3(1): 90-118.

doi: 10.3934/GF.2021006

[10]

Rupsha Bhattacharyya .

Green finance for energy transition, climate action and sustainable development: overview of concepts, applications, implementation and challenges. Green Finance, 2022, 4(1): 1-35.

doi: 10.3934/GF.2022001

Abstract

Finance has an important influence on technological innovation (TI). There are several stages of, as well as various financial constraints on, TI. In this article, we divide TI into four stages: the development, growth, maturity, and decline stages. Concurrently, we classify TI funding sources into five types: enterprise funds, government funds, venture capital funds, loans from financial institutions, and capital market funds. Based on the analysis of the stages and financing constraints of TI, this paper constructs a state-space model to study the effects of various funding sources on TI in Hebei Province, China, from 2005 to 2018. The results show a long-term equilibrium relationship between finance and TI, whereby different financial methods have different effects on each stage of TI. Enterprise funds play a primary role in the development, growth, and maturity stages. Government funds play a prominent role in the development and growth stages. Capital market funds and loans from financial institutions only play a role in the maturity period. The role of capital market funds was positive, while that of loans from financial institutions was negative. The effect of venture capital was not noticeable at any stage. Finally, we give our conclusions and put forward some countermeasures and suggestions to promote TI in Hebei Province.

1.

Introduction

The Chinese economy has shifted from a rapid growth model to a stage of high-quality development. It is crucial that its development pattern is transformed, its economic structure is optimised, and transformation of the driving growth force occurs. In this process, technological innovation (TI) plays an important role. TI is a high-risk activity that promotes technical progress and faces a considerable risk of failure (Nanda et al., 2016). TI is the key to high-quality economic development, and finance will promote TI. Finance can guide the flow of innovation resources and promote the rational allocation of innovation elements. Schumpeter (1934) was the first to link finance and TI. He believed that innovation, as a decisive economic development factor, was essentially the result of the recombination of production factors. On the other hand, finance provides the necessary support for reallocating resources and promoting TI.

Based on Schumpeter's innovation theory, much literature has examined the interrelations and effects of the financial system and TI, believing that finance plays a driving role in TI. Greenwood and Jovanovic (1990) believed that financial institutions give full play to their advantages in information processing. While effectively reducing costs, they can screen the most promising innovative technologies, strengthen resource allocation, and promote TI. Levine (1991) and Saint-Paul (1992) believed that the uncertainty of the research and development (R & D) process exposes companies to huge intertemporal risks, and the existence of financial markets can diversify this risk, enable companies to choose more specialised technologies, and improve the success rate. King and Levine (1993) investigated the financial system and TI by constructing an endogenous growth model. They believed that a better financial system would improve the probability of successful innovation and accelerate economic development. Much evidence suggests that financial systems are important for productivity growth and economic development. Chowdhury et al. (2012) demonstrated the contrast between developed and emerging economies. They applied three distinct approaches: the ordinary least square method, cross-country instrumental variable regression approach, and panel regression method. They found that financial market development significantly contributes to the effectiveness of total R & D investment. Furthermore, this finding remains robust across different model specifications and individual estimation methods. Perez (2013) presented an alternative model of the emergence and propagation of technological revolutions. It proposed an explanation for the clustering and the spacing of technical change in successive revolutions. It provided arguments for the recurrence of clusters of bold financiers together with clusters of production entrepreneurs and an interpretation of major financial bubbles as massive episodes of credit creation, associated with the process of assimilation of each technological revolution. It concluded by demonstrating that financial capital plays a fundamental role in the articulation and propagation of technological revolutions. Many other scholars, such as Dosi (1990), Giudici et al. (2000), Andrew (2007), Zhu et al. (2008), Yu (2013), Zhang et al. (2015), and Audretsch (2016), have established the important role of various dimensions of financial development in TI. Some scholars also believe that the relationship between finance and innovation is more complicated. Law et al. (2018) examined the non-linear relationship between financial development and innovation using generalised method of moments (GMM) estimators for a panel data model for 75 developed and developing countries from 1996 to 2010. An inverted U-shaped non-linear relationship between finance and innovation was observed. This finding implies that finance enhances innovation only up to a certain level. Beyond that level, further development of finance tends to affect innovation adversely.

There are various financing methods in the financial market, which have various influences on TI. In the 1980s, the evidence suggested that venture capital not only played a significant role but that it was a unique kind of investment in terms of when, where, and how it was done (Economics, 1983). However, other research indicates that the "capital" in venture capital is the least important ingredient in fostering TI (Timmons et al., 1986). Since then, research has expanded on the effects of different financial modes on TI. Some scholars, such as Stulz (2000), Legrand et al. (2010), and Amore et al. (2013), have conducted studies on the banking system. Their results showed that banks could monitor loans to science and technology enterprises and promote scientific and technological progress, as well as economic growth, through regional diversification. Considering the financing difficulties of private enterprises, Zhu et al. (2021) studied the impact of financing methods on TI. The results show that internal financing can promote TI behaviour more than external funding. Among various external funding forms, bank loans have the most significant influence on TI among private enterprises. Rin et al. (2006), Atanassov et al. (2007), and Liao et al. (2019) studied capital markets. They believed that the second-board market was conducive to increasing investment in small- and medium-sized technological enterprises and innovative start-ups in the start-up stage. The development level of the capital market had a pronounced effect in promoting TI. Bejakovic (2002), Kaplan et al. (2003), Dushnitsky and Lenox (2005), and Zhang et al. (2020) studied the roles of venture capital in R & D and TI. They noted that venture capital can solve the information asymmetry, credit risk, and high financing costs inherent in TI. At the same time, it can provide financial support for scientific and technological enterprises in the development period and promote their rapid development. Lerner et al. (2020) recognised the role of venture capital in promoting innovation and analysed the limitations in promoting substantial technological changes. Zhang et al. (2019) compared the effects of equity financing and debt financing on TI. The findings showed that equity financing, which has higher risk tolerance, has a more positive impact on innovation than debt financing in terms of both economic uptrend and economic downtrend, and that government efficiency plays a significant role in supporting the performance of TI.

In recent years, some scholars have also begun to notice the stages of TI, studying the effects and functions of different financing methods on different TI stages. From the three stages of R & D input, achievement transformation, and industrial output, Zheng et al. (2015) established a variable parameter state-space model. They analysed the service path and examined the effectiveness of the financial sector for TI. Gao (2017) divided TI into three development stages: R & D, achievement transformation, and industrialisation. Using panel data from 2007 to 2016, he conducted an empirical test on science and technology finance and TI in Henan Province. His results showed that the impact was quite different. Pu et al. (2017) divided TI into three stages: TI, technological transformation, and high-tech industrialization, and also divided financial technology into two aspects: public financial technology and financial market technology. Then he analysed the impact of financing on technology in different TI stages.

To date, many researchers have mainly studied the one- or two-way interactions between finance and TI. In recent years, a few studies have noticed the stages of TI. Still, due to inconsistent divisions of TI stages, significant differences emerge in research results. Moreover, starting with the TI stages, it is rare to consider the effects of different sources of funds on the different stages of TI. In a relatively mature study on the stage division of technology innovation, Markard (2020) systematically analysed the stages of technology innovation system (TIS), introduced the key elements of the TIS life cycle framework, and distinguished between the four key stages: formation, growth, maturity, and decline. TI consists of several stages. The activities in different stages have various financing constraints and suitable financing methods. This is an important entry point and provides space for writing this article.

TI consists of several stages, each of which often uses different financing methods. However, the literature on the effects of financial methods in various TI stages is scarce, which provided space for the analysis detailed in this paper. This paper's main contributions are as follows: first, based on analysing the financing methods in different stages of TI, this paper studies the effects of different financing methods in different stages of TI by establishing a state-space model; second, this paper chooses Hebei Province, which is relatively backward in terms of financial development and TI, as the research object, which is unique in the existing research.

China has a vast territory and a large population. Following 40 years of rapid development after reform and opening up, China is facing great pressure from the transformation of growth drivers and economic structure. We chose Hebei Province as the sample, as it has some economic characteristics that are similar to those of the whole country. Hebei Province is located in North China, surrounding the two municipalities of Beijing and Tianjin. Before 2015, Hebei Province had long been among the most prosperous provinces in China, ranking sixth for GDP. However, due to its historical conditions, Hebei has a relatively high proportion of steel, cement, and other enterprises with high energy consumption and pollution. With the increasing requirements for environmental protection in recent years, Hebei Province has experienced an intensified industrial structure adjustment, and, consequently, its economic growth has slowed. Its GDP ranking declined to thirteenth in 2018. Hebei Province is now facing tremendous pressure due to economic transformation. Therefore, Hebei must strengthen its TI, in order to promote industrial structure adjustment and transform its economic growth mode, which is very similar to China's overall economy. Taking Hebei Province as the study object thus reflects the current circumstances of China's high-quality development. This article has a certain referential role in exploring the use of finance to support TI and promote China's economic transformation.

The rest of this paper is structured as follows: the second part analyses the stages of TI, and the financing methods and applicability of TI, which provides the theoretical analysis of this paper; the third part constructs the evaluation index system and theoretical model of financing methods to promote TI; in the fourth part, combined with the data of Hebei Province from 2005 to 2018, the above theoretical model is empirically tested; the fifth part analyses the results of the empirical test; and the sixth part summarises the conclusions and makes corresponding suggestions.

2.

TI stages and financing methods

2.1. Stages of TI

TI is a complex activity with greater uncertainty, and it is affected by many factors (Siming et al., 2019). Rosenberg (2009) believes that innovation is a complex and uncertain process in which many changes will occur. A model that describes innovation as a smooth linear process will give a seriously misleading picture of the nature and direction of the causality. In enterprises, technology and products are closely integrated, and TI is often concentrated in related product innovation. Therefore, based on the product life cycle theory (Vernon, 1966), and combined with the analysis of Markard (2020), this article divides TI into four stages according to the technological maturity of the products: development stage, growth stage, maturity stage, and decline stage. At each stage, the market performance of related technological products presents different characteristics.

The development stage is the R & D phase of new technology, where there is no similar technology or related technical product on the market. In this stage, much money often needs to be invested into developing the new technology; thus, this is an investment stage without any return. The technology has not yet been transformed into products, and few enterprises are involved, with less competitive pressure in the market. In the latter part of this stage, new products are gradually created and introduced to the market, and then TI enters the next stage-the growth stage. In the growth stage, the new products featuring the latest technology are introduced into the market rapidly. These products are also updated quickly, with product models and specifications also changing. In this stage, the production, sales, and profits of new products multiply, while market awareness is gradually improved. In this period, the product technology has passed the development stage. However, as the new product forms progressively, it still needs research and development financing in order to meet market needs. Simultaneously, due to the rapid growth of the product market and profit, other manufacturers may also seize business opportunities and develop similar products, resulting in the emergence of market competitors. Otherwise, the product market expands vastly, such that there is less competitive pressure. At this stage, although the new product is profitable, the profit is small. Due to the high cost of early R & D investment, the overall profit is still low or even negative. After the growth period, TI enters the maturity stage. The market penetration rate of new products is relatively high, and both the technical specifications and sales volume of products are stable. The product technology becomes very mature, such that there is no need for significant technical improvement. Less research and lower development costs are needed to maintain the necessary technological advancement. Many manufacturers may be producing the product at this stage, their profit margins generally being low and decreasing. At this stage, the technology is relatively mature; the R & D cost is low; and the sales of new products are stable, so the overall profit is high.

In the decline stage of TI, products face problems such as obsolete models and outdated functions. The sales volume drops significantly, and the technology becomes outdated, gradually being eliminated and replaced by another new product. No extra capital will be invested in the product, but, instead, another new product will emerge to start a new round of TI. Considering the particularity of this stage, this paper will not conduct a later analysis of the decline stage of TI.

2.2. Financing methods of TI

Traditionally, there have been three main sources of funds for TI of Chinese enterprises: enterprise funds, government funds, and loans from financial institutions (Liang et al., 2009). With the development of the capital market, financing channels such as the GEM (Growth Enterprises Market), STAR Market (Science and Technology Innovation Board), New OTC (Over the Counter) Market are increasingly unimpeded. At the same time, venture capital in recent years has also expanded the funding sources of TI. At present, there are five main financing methods in China: enterprise funds, government funds, venture capital funds, loans from financial institutions, and capital market financing (Song et al., 2015).

Enterprise funds are the enterprise's capital that comes from its business profits. These can be used freely and at no additional cost. In recent years, enterprise funds have accounted for more than 70% of China's R & D spending, ① making them the most important TI capital source. By investing in TI, enterprises have fewer restrictions and can apply in all stages. Therefore, in terms of quantity, enterprise funds are the primary source of funds. Government funds are financial resources allocated by the government to enterprises. Given their status as technology development projects encouraged by the government, the cost of funding through government funds is lower. Usually, government funds are much smaller than enterprise funds, making them not necessarily the primary funds. However, government funds reflect the government's policy guidance and guide other funds, making them a significant source of funds. Venture capital funds are private equity investment, whereby such funds mainly invest in the initial stage of enterprises and obtain their equity. Venture capital favours science and technology enterprises which grow rapidly. The cost of the funds is lower within the agreed period. In most cases, venture capital funds do not invest explicitly in TI. However, the target companies invested in are generally innovative and have high science and technology levels. Thus, these are also an essential capital source of funds. Loans from financial institutions are a traditional financing method for enterprises. To obtain such funds, enterprises need to meet certain conditions, such as stable production and operation, mature technology, mortgaged property, and so on. Many enterprises in the initial stage cannot meet strict financial supervision and guarantee conditions, so it is difficult to obtain the loans. The use of loans generally requires the payment of agreed-upon interest, as well as some other fees, such that the service cost is typically high. Capital market funds are a way to obtain funds from the securities market by issuing securities. At present, China's multi-level capital market system is becoming more and more mature. A multi-level capital market system has formed with the Shanghai and Shenzhen's main board as the main market and the Growth Enterprise Market, the New Third Board, and the Science and Technology Innovation Board as the auxiliary boards. The securities issued in Shanghai and Shenzhen's main board market are generally for enterprises with stable production and operation, mature technology, and standardised management, which is an important source of production and operation funds for modern enterprises. Since the GEM, New Third Board, and Science and Technology Innovation Board are mainly for financing of small and medium-sized and TI enterprises, they can effectively alleviate the lack of enterprise technology innovation funds, so they have become important sources of enterprise TI funds.

According to the above analysis, five financing funds are available for TI. There are different technological risks in different TI stages, which restrict the source of funds (Song et al., 2015; Sasidharan et al., 2015) and lead to the adoption of different financing methods in different stages.

TI is characterised by high risk and low return. In the development stage, TI faces a more significant risk of failure and requires more capital investment. The capital is required to achieve a lower cost and a more vital ability to resist threats. Therefore, enterprises mainly rely on their self-funds, government funds, and venture capital funds. In the growth stage, the market value of innovative products becomes apparent. In this stage, enterprises gradually normalise their operations, enhance their profitability, and expand their funding sources. These funds generally include enterprise funds, government funds, venture capital funds, and loans from financial institutions. As the technological products become more profitable, the proportion of loans from financial institutions may increase. Under certain conditions, capital markets such as the Growth Enterprise Market, the New Third Board, and the Science and Technology Innovation Board have also begun to provide financing for growth-stage enterprises, which has become an important financing method. In the mature stage of TI, the technical performance of products becomes stable enough, the market share becomes higher; the profitability of products is stronger; and the enterprise management becomes more standardised. At this stage, venture capital and government funds gradually withdraw. The funding sources mainly include enterprise funds, loans from financial institutions, capital market funds, and so on.

Once TI enters the decline stage, the product's performance starts to lag; its function gradually ages; the market share declines; and it faces elimination. TI focuses on developing new products in this stage; that is, another round of new technologies and new products begins. Considering the case, the analysis of this paper does not take the decline stage into account. It only studies the development, growth, and maturity stages of TI.

From the above theoretical analysis combined with Table 1, it can be seen that the different characteristics affect the choice of financing methods. Generally, enterprise funds can be applied to all stages of TI; government funds, venture capital, and some capital market funds will play a role in the development and growth stages; loans from financial institutions and capital market funds are mainly invested in the growth and maturity stages. However, whether the various sources of funds for TI in Hebei Province have played their due role requires testing through an empirical model.

Table 1.

The stages of TI and the financing methods.

Stages of TI

Financing methods

Development stage

Enterprise Funds, Government Funds, Venture Capital Funds

Growth stage

Enterprise Funds, Government Funds, Venture Capital Funds, Loans from Financial Institutions, Capital Market Funds

Mature stage

Enterprise Funds, Loans from Financial Institutions, Capital Market Funds

This article focuses on analysing the effects of different financing methods on TI, so we need to choose indicators according to two aspects. One is the source of funds, and the other is TI output. For the sources of funds, on the basis of the previous analysis, we selected five indicators: enterprise funds, government funds, venture capital funds, loans from financial institutions, and capital market funds. For the outputs of TI, each stage has different characteristics and various achievements. New technologies are developing in the development phase, such that there is no product and no profitability. The achievements are usually in R & D projects. Therefore, we selected the number of R & D projects as the achievements. During the growth stage, innovation results began to emerge, and new products come out. However, due to the large investment required in the early stage, the product profit is still insufficient. The innovation output is usually in the form of intellectual property. Thus, we take the number of patent applications as innovation results. In the mature stage, innovative products are produced with higher market share and better profitability. Therefore, innovation achievement was assessed as the product's economic value, that is, the sales revenue of a new product.

According to the above analysis, the indicators of financial development and TI achievements selected for this paper are shown in Table 1.

In Table 2, the indicators X1 (enterprise funds), X2 (government funds), and X4 (loans from financial institutions) were obtained from the data on the amount of funding for science and technology in the annual Hebei Economic Yearbook. X3 (venture capital funds) was replaced by the venture capital scale managed in Hebei, appropriately sorted, and calculated: these data were from the annual China Venture Capital Yearbook. X5 (capital market funds) came from the data of technology companies in Hebei, as listed on the Shanghai and Shenzhen stock exchanges. This included the technology companies on the main board and all companies listed on the GEM board. The financing amount was adjusted, according to the High-tech Industries Catalog published by the National Bureau of Statistics. The three indicators of achievements (Y1, Y2, and Y3) were obtained from the Hebei Statistics Yearbook of Science and Technology and China Statistics Yearbook of Science and Technology. Since China's venture capital industry was not developed at the start of this century, according to the existing statistics, the earliest year for which venture capital data can be collected is 2005. So the time interval of all the above indicators was from 2005 to 2018.

Table 2.

The evaluation index system.

Category

Indicators

Unit

Symbol

Symbol after the logarithm

Financial Methods

Enterprise Funds Government Funds Venture Capital Funds Loans from Financial Institutions Capital Market Funds

ten thousand yuan

X1 X2 X3 X4 X5

LX1 LX2 LX3 LX4 LX5

TI achievements

Number of R & D Projects Number of Patent Applications Sales Revenue of New Product

Through descriptive analysis, we can have a preliminary understanding and grasp of variables. Table 3 shows the descriptive statistics of each variable after eliminating the price factor. In terms of the explanatory variables, the average value of enterprise funds is the largest, which is much larger than other types of funds; the average values of government funds (X2) and financial institution credit funds (X4) are small, at only 2.88% and 0.98% of enterprise funds, respectively. The data in the table also show that the volatility of venture capital funds (X3) is relatively large, and the coefficient of variation exceeds 2. The volatility of other variables is relatively small.

This paper mainly studies the effect of different sources of financing on TI. Based on the foregoing analysis, it can be seen that every financing method has restriction conditions, and the financing methods that can be adopted at each stage are also different. With the development of technology, the stage of TI will change, and the effects of every financing method will not be the same. In order to reflect the changing effect, the variable parameter state space model can be used for research. By studying the changes of model parameters over time, the effects of every financing method on TI stages can be reflected.

Based on the Cobb-Douglas production function, the form of the variable parameter state-space model is as follows:

(1)

(2)

where i = 1, 2, 3 represents the development stage, growth stage, and maturity stage of TI, respectively; t is the time, with value range of 2005–2018; represents the achievements of the three stages of TI each year-namely, the number of R & D projects, the number of patent applications, and the sales revenue of new products; represents enterprise funds, government funds, venture capital, loans from financial institutions, and capital market funds, respectively; is a variable parameter, indicating the effect of different forms of investment on TI in each stage (namely, the effective coefficient)-the larger the value is, the better the financial support effect will be; and and are the corresponding random error terms.

4.

Empirical test of the model

4.1. Stationarity and co-integration test

The variables selected were all time-series data. Heteroscedasticity was eliminated by taking the logarithm. The ADF unit root test was performed on the variables, in order to avoid false regression. The results of the stationarity test are shown in Table 4.

Table 4.

Stationarity test.

Variables

Test form

ADF statistics

5% critical value

Stationarity

LX1

(C, N, 0)

−2.8239

−3.0810

No

△LX1

(C, T, 0)

−5.6778

−3.7912

Yes

LX2

(C, T, 0)

−1.6767

−3.7597

No

△LX2

(N, N, 0)

−2.9936

−1.9684

Yes

LX3

(C, N, 1)

−1.4562

−3.0989

No

△LX3

(N, N, 0)

−2.2677

−1.9684

Yes

LX4

(C, N, 1)

−2.3256

−3.0989

No

△LX4

(N, N, 0)

−2.1784

−1.9684

Yes

LX5

(C, N, 1)

−1.8031

−3.0989

No

△LX5

(C, N, 0)

−7.2057

−3.0989

Yes

LY1

(C, T, 0)

−2.4127

−3.7597

No

△LY1

(C, N, 3)

−2.8689

−2.7290*

Yes

LY2

(C, T, 0)

−2.0013

−3.7597

No

△LY2

(N, N, 0)

−3.7684

−1.9684

Yes

LY3

(C, N, 0)

−2.9483

−3.0810

Yes

Note: The test forms (C, T, K) mean that the test equation includes constant term (C), time trend (T), and the order of the lag term. N means no C or T, respectively. △ is the difference operator.

The test results indicate that only LY3 was a stationary series among all the eight variables, while the other variables were first-order integral series. Then, we used the Johansen co-integration test to determine the long-term equilibrium relationships between TI variables and financial variables. The test results are shown in Table 5.

Table 5.

Co-integration test of output variables and financial variables.

The results in Table 3 indicate that there was at least one co-integration relationship between each output variable and the financial variables, indicating that finance has a significant long-term effect on TI. However, the analysis only shows that different TI stages are affected by financial variables; we established the state-space model to analyse the influences of the financial variables on TI.

4.2. Empirical results of the model

It will take some time for finance to play a role in TI. In this paper, state-space models were established, where the lag-periods were set as one year. In each equation, LY1, LY2, and LY3 were the explained variables and the financial variables-namely, X1, X2, X3, X4, and X5-were the explanatory variables. We use Eviews11.0 to get the estimation and test results of each model. After multiple operations and adjustments, each model's estimation and test results are shown in Table 6. The initial models gave the estimated results with all five financial variables, while the final model gave the estimated results after removing the insignificant variables. In the table, C(1) are the coefficients of constant terms, and C(2) are the exponential values of random error term variance. SV(1)–SV(5) are the dynamic parameter values of the five variables (i.e. LX1, LX2, LX3, LX4, and LX5). Only the parameter values of the last year (2018) are listed in Table 6, and all the dynamic parameter values of each final model in every year are shown in Table 7.

Table 6.

The estimated results of the models.

Parameter

LY1 (development stage)

LY2 (growth stage)

LY3 (maturity stage)

Initial model

Final model

Initial model

Final model

Initial model

Final model

Coefficient values

C(1)

2.3591(0.9317)

1.5878(0.7975)

−4.0103(−4.4421)*

−4.1364(−5.5004)*

3.4850(6.8625)*

3.7282(12.7510)*

C(2)

−3.7168(−10.4641)*

−3.8986(−9.8832)*

−5.0390(−8.1404)*

−4.9115(−8.5220)*

−5.4609(−6.7240)*

−5.6389(−13.4142)*

Final value of dynamic parameter

SV(1)

0.1875(1.4410)

0.2423(3.7790)*

0.5557(8.2735)*

0.6351(11.3461)*

0.9507(17.4790)*

0.9306(799.8982)*

SV(2)

0.3502(1.7952)**

0.3766(4.2495)*

0.3893(3.8652)*

0.3216(3.2761)*

0.0057(0.0697)

—

SV(3)

0.0156(0.3114)

—

0.0399(1.5460)

—

0.0225(1.0772)

—

SV(4)

−0.059674(−0.8305)

—

−0.1562(−4.2115)*

−0.1370(−3.6404)*

−0.0233(−0.7768)

—

SV(5)

0.054959(0.7202)

—

0.1773(4.4997)*

0.1732(4.1240)*

−0.0095(−0.2967)

—

Note: The figures in square brackets under the estimated coefficients are the corresponding Z-statistics. *, **, and *** indicate that the coefficient is significant at the significance level of 0.01, 0.05, and 0.10, respectively.

The results in Table 6 show that compared with the initial model, the effect of each final model has been significantly improved; the Log likelihood has been significantly improved; and the statistics of AI, SC, and HQ have also been significantly reduced. C(2) of each model and C(1) of LY2 and LY3 models passed the significance test. Although C(1) of model LY1 did not pass the test, it did not affect the analysis. The state equation of each initial model has one or more dynamic parameters that failed the test; the final model was obtained after removing insignificant variables; each parameter passed the significance test at the level of 0.01. Overall, the effects of each final model are very good.

To ensure the robustness of the model and reduce the impact of sample time selection as much as possible, the two-year samples in 2005 and 2018 are removed and the time interval from 2006 to 2017 is re-estimated. The results indicate that the estimation results are basically consistent with the above conclusions, indicating that the research conclusions in this paper are relatively robust.

5.

Analysis of results

5.1. Variable parameter analysis of the development stage

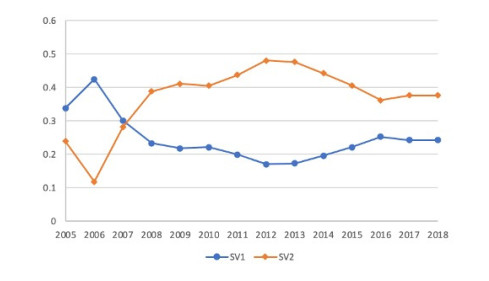

In the development stage, innovation achievements were represented by the number of R & D projects (LY1). The estimation results showed that, in the initial model, only the variable parameter of government funds (SV2) passed the significance test. After the insignificant variables (LX3, LX4, and LX5) were removed, the parameters SV1 (enterprise funds) and SV2 (government funds) passed the significance test in the final model. These results indicate that, in the development stage of TI in Hebei Province, enterprise funds and government funds play prominent roles. Figure 1 shows the changes in the parameters with respect to time.

Figure 1.

Dynamic parameter chart of enterprise funds and government funds.

Figure 1 shows that, in the development period, enterprise funds and government funds significantly promoted output, while the elasticity coefficient was remarkably positive. In the early part of the sample period (2005–2007), the elasticity coefficients of enterprise funds were greater than those of government funds. In 2008, the elasticity coefficients of government funds began to surpass those of enterprise funds.

The reasons for this are closely related to China's national technology innovation policy. In 2005, the State Council of China issued the Outline of the National Medium- and Long-term Plan for Scientific and Technological Development (2006–2020), proposing that China should become an innovation-oriented country by 2020 and a global scientific and technological power by the middle of the 21st century. The government has increased its support for TI, such that government funding invested in TI of enterprises has increased significantly, which played a vital guiding role. Furthermore, government funding for TI has a clear purpose and strict requirements, such that their effects are better than enterprise funds. In addition, industrial enterprises above a designated size in Hebei are dominated by heavy industries, such as steel, cement, and chemical industries, which have low profit margins. The Chinese government has implemented many environmental protection policies, such as production transformation, energy conservation, emissions reduction, and other requirements in recent years, which decreased enterprise profits and, thus, TI funds. Therefore, the dynamic parameters SV2 were significantly higher than the parameters SV1.

According to the previous theoretical analysis, funding sources in the development stage were mainly enterprise funds, government funds, and venture capital. Little access is available to loans from financial institutions or funds from the capital market. Thus, their effects were not significant, consistent with the theoretical analysis in this paper. The empirical study here also shows that the role of venture capital was not significant; the reason why will be specifically analysed later when it comes to venture capital.

5.2. Variable parameter analysis of the growth stage

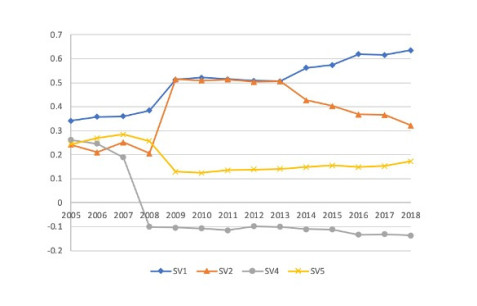

In the growth stage, innovation achievements are represented by the number of patent applications (LY2). The initial model estimation result shows that only the parameter of venture capital (SV3) failed the significance test. After it was removed, the final model included four variables, with every parameter being highly significant. The results indicate that enterprise funds (SV1), government funds (SV2), loans from financial institutions (SV4), and financing in the capital market (SV5) play significant roles. However, the effect of each variable was different (see Figure 2).

Figure 2.

Dynamic parameter charts in the growth stage.

Considering Figure 2, the sample period can be divided into three stages:

(1) Before 2008, the four financial methods all had a noticeable effect on the TI output. SV1 was the highest, between 0.35 and 0.4; meanwhile, the others showed little difference, almost all between 0.2 and 0.3.

(2) From 2008 to 2013, the effects of various financial methods diverged. SV1 and SV2 increased significantly, both exceeding 0.5. However, SV5 and SV4 decreased significantly, the former dropping to around 0.15 and the latter stabilising after dropping to below −0.1.

(3) After 2014, SV1 and SV2 also began to diverge. SV1 improved further, from 0.5 to more than 0.6. SV2 began to decline gradually, from around 0.5 to about 0.3. During this period, the roles of financing in the capital market and loans from financial institutions were relatively stable.

During this period, there were many reasons for the variation in the effects of financial modes. First, during the growth period, the impact of TI begins to appear, and the innovation achievements-the number of patent applications (LY2)-increase rapidly. At the same time, with the rise of new products and profits, enterprises will also have more money to invest in TI, promoting their funding effect. Second, the Outline of The National Medium- and Long-term Scientific and Technological Development Plan (2006–2020)② was promulgated in 2005. After several years, the implementation effect began to emerge, and the elasticity coefficients of SV1 and SV2 were improved. Third, to deal with the outbreak of the subprime mortgage crisis in the United States in 2008, the Chinese government offered greater convenience and preferential treatment to enterprises with respect to bank loans and capital market funds. The amount of the loans exceeded the needs of the businesses. Further, limited by data sources, the data of capital market funds (Y5) used in this paper were the total enterprise funds from the capital market. Although the enterprises were all TI-oriented enterprises, only some of the funds are generally used for TI. Therefore, the effect was lower than that of the enterprise funds and government funds. Fourth, taking loans from financial institutions (X4) is a traditional way to obtain funds. In China, the innovation environment in Hebei Province is not advanced, and so science and technology loan policies are not perfect. For risk control, fewer loans are applied to TI, and more restrictive conditions are required, such as requiring collateral or guarantees. This leads to a squeeze on enterprise resources and may be another important reason for the negative effect observed (SV4). Fifth, after 2014, the output elasticity of government funds (SV2) dropped significantly, which may be related to the financial strain caused by the economic transformation of Hebei Province. Under the pressure of environmental protection policies, the economic growth of Hebei Province began to slow. The average annual GDP growth rate was above 10% before 2012, dropping to 6.5% in 2018. Its GDP ranking fell from 6th in 2012 to 13th in 2018. This slowing of economic growth led to a sharp decrease in fiscal revenue. The funds applied to TI dropped from 918 million yuan in 2015 to 550 million yuan in 2018. Before 2014, government funds typically accounted for less than 3% of enterprise funds, then decreased rapidly to 1.48% in 2018. The proportion of government funds to enterprise funds is relatively low. In the face of such large fluctuations, the effect of government funds declined and was significantly lower than that of enterprise funds.

5.3. Variable parameter analysis of the mature stage

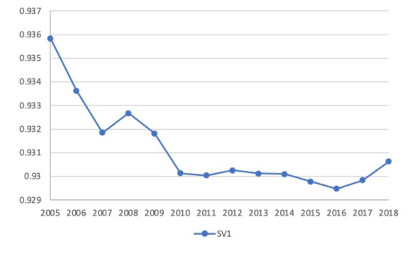

Only the enterprise funds (X1) in the initial model passed the significance test in the maturity stage (see Table 1). After insignificant variables were eliminated, the final model retained the independent variable (X1). Figure 3 shows the variation of the parameter SV1.

Figure 3.

Dynamic parameter chart during the maturity period.

In this stage, the technology is mature; the product sales volume is large; and the profit is relatively stable. In this period, significant investment in TI is not required; expenses are to cover the cost of providing technical support for functional stability. The elasticity coefficient fluctuated at a high level (around 0.93) during this period.

5.4. Comprehensive evaluation

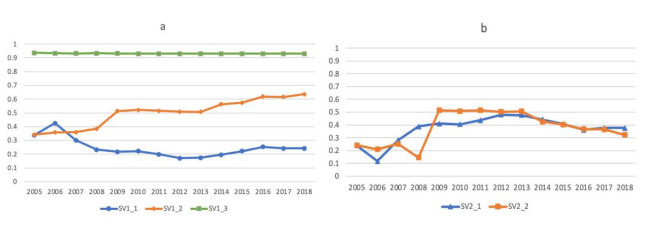

From the previous analysis, it can be seen that at different TI stages, the roles of the financial methods are not the same. Enterprise funds (X1) play an essential role in all three phases, while government funds (X2) were important in the development and growth stages. Loans from financial institutions (X4) and capital market funds (X5) played a role only in the growth stage. Figure 4 shows the changes of SV1 and SV2. The underlined numbers 1, 2, and 3 represent the development, growth, and maturity stages, respectively.

Figure 4.

Dynamic parameter charts of enterprise funds and government funds.

Figure 4(a) shows that SV1, in the maturity stage, was stably above 0.9, significantly higher than in the development and growth stages. Except for in 2006, the SV1 of the growth period was higher than in the development period. SV1 was the lowest and fluctuated during the development period. This indicates that enterprise funds play different roles according to the TI stage. The elasticity coefficient increases from development to maturity, and the effect becomes more and more significant. Figure 4(b) shows that the effects of government funds (X2) were noticeable in both the development and growth stages. The trend was nearly the same, except that it fluctuated slightly in the growth period. The results also showed that venture capital funds did not play a significant role in the three stages. The venture capital industry in Hebei is undeveloped. The venture capital scale in Hebei accounts for less than 1% of the whole country's venture capital. In 2018, the scale was 19.83 billion yuan, only 0.22% of the total national scale of 89,969.55 billion yuan. In addition, in the sample period, venture capital funds accounted for less than 8% of the total funds, on average, with significant fluctuation year by year. It can be seen that venture capital had not become the main fund for TI in Hebei and that its effect on TI was not significant.

6.

Conclusions and recommendations

By constructing a state-space model, we took Hebei Province as an example, in order to study the influence of five financial methods on three stages of TI. In terms of economic strength, Hebei Province is a mid-ranking Chinese province, but its TI ability is weak. Hebei has also faced significant pressures in recent years, such as structural adjustment and economic transformation. Thus, Hebei Province serves as a microcosm of China. Making Hebei Province the object of inquiry allows for a representative picture of the role of different financing methods on TI under the pressure of economic transformation in contemporary China.

Subsequent to our analysis, we can draw the following main conclusions: (1) Different financial methods in Hebei Province have various effects in every TI stage. These differences were clearly noticeable in the research results. (2) In the development stage, enterprise funds and government funds played essential roles. The effect of government funds was more significant than that of the enterprise funds. (3) In the growth stage, enterprise funds, government funds, and capital market funds all play important roles. Their effect decreased successively. Affected by various factors, the impact of loans from financial institutions was negative. (4) In the maturity stage, only enterprise funds played an important role. (5) Among all five financial methods, only enterprise funds, being the primary capital source, played an important role in all stages. Government funds played important roles in the development and growth stages, which are crucial to support TI. Capital market funds only played a role in the growth period, with their function being smaller than that of enterprise funds and government funds. Loans from financial institutions only played a role in the growth stage; however, the effect was negative. Venture capital was not an influential fund source, and its role in each step was not apparent.

On the basis of the above research conclusions, in order to promote TI in Hebei Province, we propose the following suggestions: (1) Promote the development of a multi-level financial market system. The multi-level and diversified financial market system can meet the financing needs and effectively promote the development of TI. (2) Pay attention to the difference in the effects of financing methods on TI and suggest that different financing methods should be adopted for TI at different stages. (3) Promote the integrated development of the financial market and the TI market and enhance the effect of TI.

Acknowledgements

The authors thank the anonymous reviewers for their constructive feedback.

Fund projects

This research was funded by the Chinese National Funding of Social Sciences (18ATJ002 and 17BTJ016), the project of Guangzhou Financial Research(16GFR02B10), and the 13th Five-year Plan of Guangzhou Social Science (2018GZYB129).

Conflicts of interest

The authors declare no conflict of interest.

References

[1]

Amore MD, Schneider C, Aldokas A (2013) Credit supply and corporate innovation. J Financ Econ 109: 835-855. doi: 10.1016/j.jfineco.2013.04.006

[2]

Andrew T (2007) The role of finance and corporate governance in national systems of innovation. Organ Stud 28: 1461-1481. doi: 10.1177/0170840607075676

[3]

Atanassov J, Nanda VK, Seru A (2007) Finance and innovation: The case of publicly traded firms. SSRN Electron J 15: 89-92.

[4]

Audretsch DB, Lehmann EE, Paleari S, et al. (2016) Entrepreneurial finance and technology transfer. J Technol Transfer 41: 1-9. doi: 10.1007/s10961-014-9381-8

[5]

Bejaković P (2002) The financing of research and development. Oxf Rev Econ Policy 18: 35-51. doi: 10.1093/oxrep/18.1.35

[6]

China Venture Capital Research Institute (2010-2018) China Venture Capital Yearbook, Beijing: China Development Press.

[7]

Chinese Academy of Science and Technology for Development (2005-2009) Venture Capital Development in China, Beijing: Economic & Management Publishing House.

[8]

Chowdhury RH, Maung M (2012) Financial market development and the effectiveness of R & D investment: Evidence from developed and emerging countries. Res Int Bu Financ 26: 258-272. doi: 10.1016/j.ribaf.2011.12.003

[9]

Dosi G (1990) Finance, innovation and industrial change. J Econ Behav Organ 13: 299-319. doi: 10.1016/0167-2681(90)90003-V

[10]

Dushnitsky G, Lenox M (2005) When do incumbents learn from entrepreneurial ventures? Res Policy 34: 615-639.

[11]

Economics V (1983) Regional Patterns of Venture Capital Investment. Prepared for US Small Business Administration. Washington, DC: Small Business Administration.

[12]

Gao H (2017) Research on the Effectiveness of Supporting Scientific and Technological Innovation by Science and Technology Finance in Henan Province—An empirical Test based on panel Model. Financ Theory Pract, 65-70.

[13]

Giudici G, Paleari S (2000) The provision of finance to innovation: A survey conducted among Italian technology-based small firms. Small Bus Econ 14: 37-53. doi: 10.1023/A:1008187416389

[14]

Greenwood J, Jovanovic B (1990) Financial Development, Growth, and the Distribution of Income. J Political Economy 98: 1076-1107. doi: 10.1086/261720

[15]

Hebei Provincial People's Government (2005-2019) Hebei Economic Yearbook, Beijing: China Statistics Press.

[16]

King RG, Levine R (1993) Finance, entrepreneurship and growth: Theory and evidence. J Monetary Econ 32: 513-542. doi: 10.1016/0304-3932(93)90028-E

[17]

Law SH, Lee WC, Singh N (2018) Revisiting the finance-innovation nexus: Evidence from a non-linear approach. J Innov Knowl 3: 143-153. doi: 10.1016/j.jik.2017.02.001

[18]

Legrand DP, Pommet S (2010) Venture capital syndication and the financing of innovation: Financial versus expertise motives. Econ Lett 106: 75-77. doi: 10.1016/j.econlet.2009.10.004

[19]

Lerner J, Nanda R (2020) Venture capital's role in financing innovation: What we know and how much we still need to learn. J Econ Perspect 34: 237-261. doi: 10.1257/jep.34.3.237

Liang L, Ma R, Tian Y (2009) R & D Financing Source and Technical Innovation—Empirical Research on China's Large and Medium-Size Industry Firms. Sci Sci Manage S T 7: 89-93.

[22]

Liao G, Drakeford BM (2019) An analysis of financial support, technological progress and energy efficiency:evidence from China. Green Financ 1: 174-187. doi: 10.3934/GF.2019.2.174

[23]

Markard J (2020) The life cycle of technological innovation systems. Technol Forecast Soc Change 153: 119407.

[24]

Nanda R, Rhodes-Kropf M (2016) Financing risk and innovation. Manage Sci 63: 901-918. doi: 10.1287/mnsc.2015.2350

[25]

National Bureau of Statistics, Ministry of Science and Technology (2005-2019) China Statistics Yearbook on Science and Technology, Beijing: China Statistics Press.

[26]

Perez C (2013) Finance and technical change: a neo-schumpeterian perspective. Financ Market Res: 76-91.

[27]

Pu Z, Tian Q, Jiangpeng Z (2017) Research on the Influence of Technology Finance on Technology Innovation. 2017 3rd International Conference on Innovation Development of E-commerce and Logistics (ICIDEL 2017), 190-194.

[28]

Rin MD, Nicodano G, Sembenelli A (2006) Public policy and the creation of active venture capital markets. J Public Econ 90: 1699-1723. doi: 10.1016/j.jpubeco.2005.09.013

[29]

Rosenberg N (2009) Studies on science and the innovation process. World Sci, 428.

[30]

Saint Paul G (1992) Technological Choice, Financial Markets and Economic Development. Eur Econ Rev 36: 763-781. doi: 10.1016/0014-2921(92)90056-3

[31]

Sasidharan S, Jijo Lukose PJ, Komera S (2015) Financing constraints and investments in R & D: Evidence from Indian manufacturing firms. Quart Revi Econ Financ 55: 28-39. doi: 10.1016/j.qref.2014.07.002

[32]

Schumpeter JA (1934) The theory of economic development; an inquiry into profits, capital, credit, interest, and the business cycle, Cambridge, Mass.: Harvard University Press.

[33]

Science and Technology Department of Hebei Province, Hebei Provincial Statistics Bureau (2005-2019) Hebei Statistics Yearbook on Science and Technology, Shijiazhuang: Hebei Science & Technology Press.

[34]

Siming L, Mengxin W, Yong T (2019) Stabilizing inflation expectations in China: Does economic policy uncertainty matter? Green Financ 1: 429-441.

[35]

Song M, Ai H, Li X (2015) Political connections, financing constraints, and the optimization of innovation efficiency among China's private enterprises. Technol Forecast Soc Change 92: 290-299. doi: 10.1016/j.techfore.2014.10.003

[36]

Kaplan SN, Strömberg P (2003) Financial contracting theory meets the real world: An empirical analysis of venture capital contracts. Rev Econ Stud 70: 281-315. doi: 10.1111/1467-937X.00245

[37]

Stulz RM (2000) Financial structure, corporate finance and economic growth. Int Rev Financ 1: 11-38. doi: 10.1111/1468-2443.00003

[38]

Timmons JA, Bygrave WD (1986) Venture capital, s role in financing innovation for economic growth. J Bus Venturing 1: 161-176. doi: 10.1016/0883-9026(86)90012-1

[39]

Vernon R (1966) International investment and international trade in the product cycle. Quart J Econ 80: 190-207. doi: 10.2307/1880689

[40]

Yu L (2013) Empirical Study on Regional Finance and S & T Innovation. Sci Sci ManageS T 34: 88-97.

[41]

Zhang C, Mao D, Wang M (2020) Role of Venture Capital in Enterprise Innovation Under Psychological Capital and Heterogeneity of Entrepreneur Capital. Front Psychol 11: 1704-1704. doi: 10.3389/fpsyg.2020.01704

[42]

Zhang L, Zhang S, Guo Y (2019) The effects of equity financing and debt financing on technological innovation: Evidence from developed countries. Baltic J Manage 14: 698-715. doi: 10.1108/BJM-01-2019-0011

[43]

Zhang Y, Zhao L (2015) The effect of sci-tech finance investment on sci-tech innovation in Chowdhury: An empirical research based on the static and dynamic panel date model. Stud Sci Sci 33: 177-184.

[44]

Zheng Y, LI Z (2015) Research on the Effectiveness of China's Financing Service for Technology Innovation. China Soft Sci, 127-136.

[45]

Zhu E, Zhang Q, Sun L (2021) Enterprise financing mode and technological innovation behavior selection: An empirical analysis based on the data of the World Bank's survey of Chinese private enterprises. Discrete Dyn Nat Soc 2021: 8833979.

[46]

Zhu Y, Chen L (2008) Research on the development of high-tech industries' finance. J Guizhou Norm Univ, 53-58.

This article has been cited by:

1.

Jinhao Liang, Xiaowei Song,

Can green finance improve carbon emission efficiency? Evidence from China,

2022,

10,

2296-665X,

10.3389/fenvs.2022.955403

2.

Minglei Zhu, Haiyan Huang, Weiwen Ma,

Transformation of natural resource use: Moving towards sustainability through ICT-based improvements in green total factor energy efficiency,

2023,

80,

03014207,

103228,

10.1016/j.resourpol.2022.103228

3.

Huayu Sun, Fanqi Zou, Bin Mo,

Does FinTech drive asymmetric risk spillover in the traditional finance?,

2022,

7,

2473-6988,

20850,

10.3934/math.20221143

4.

Yanling Li, Mengxin Wang, Gaoke Liao, Junxia Wang,

Spatial Spillover Effect and Threshold Effect of Digital Financial Inclusion on Farmers’ Income Growth—Based on Provincial Data of China,

2022,

14,

2071-1050,

1838,

10.3390/su14031838

5.

Zhen Fang, Can Yang, Xiaowei Song,

Construction of influencing factor model for high-quality green development of Chinese industrial enterprises,

2022,

10,

2296-665X,

10.3389/fenvs.2022.1006224

6.

Lizhao Du, Xinpu Wang, Jie Peng, Gaoyang Jiang, Suhao Deng,

The impact of environmental information disclosure quality on green innovation of high-polluting enterprises,

2022,

13,

1664-1078,

10.3389/fpsyg.2022.1069354

7.

Mingxia Zhang, Mingyue Du,

Does environmental regulation develop a greener energy efficiency for environmental sustainability in the post-COVID-19 era: Role of technological innovation,

2022,

10,

2296-665X,

10.3389/fenvs.2022.978277

8.

Weilong Wang, Xiaodong Yang, Jianhong Cao, Wenchao Bu, Abd Alwahed Dagestani, Tomiwa Sunday Adebayo, Azer Dilanchiev, Siyu Ren,

Energy internet, digital economy, and green economic growth: Evidence from China,

2022,

1,

29497531,

100011,

10.1016/j.igd.2022.100011

9.

Mengxin Wang, Yanling Li, Gaoke Liao,

Spatial Spillover and Interaction Between High-Tech Industrial Agglomeration and Urban Ecological Efficiency,

2022,

10,

2296-665X,

10.3389/fenvs.2022.829851

10.

Zhenghui Li, Hanzi Chen, Bin Mo,

Can digital finance promote urban innovation? Evidence from China,

2022,

22148450,

10.1016/j.bir.2022.10.006

11.

Xianghua Yue, Shikuan Zhao, Xin Ding, Long Xin,

How the Pilot Low-Carbon City Policy Promotes Urban Green Innovation: Based on Temporal-Spatial Dual Perspectives,

2022,

20,

1660-4601,

561,

10.3390/ijerph20010561

12.

Zhenghui Li, Zimei Huang, Yaya Su,

New media environment, environmental regulation and corporate green technology innovation:Evidence from China,

2023,

119,

01409883,

106545,

10.1016/j.eneco.2023.106545

13.

Li Xu, Ping Guo, Guoqin Pan,

Effects of inter-industry agglomeration on environmental pollution: Evidence from China,

2023,

20,

1551-0018,

7113,

10.3934/mbe.2023307

14.

Xuesen Cai, Xiaowei Song,

The nexus between digital finance and carbon emissions: Evidence from China,

2022,

13,

1664-1078,

10.3389/fpsyg.2022.997692

15.

Xiaoli Hao, Yuhong Li, Siyu Ren, Haitao Wu, Yu Hao,

The role of digitalization on green economic growth: Does industrial structure optimization and green innovation matter?,

2023,

325,

03014797,

116504,

10.1016/j.jenvman.2022.116504

16.

Jianhong Cao, Siong Hook Law, Abdul Rahim Abdul Samad, Wan Norhidayah W. Mohamad,

Internal mechanism analysis of the financial vanishing effect on green growth: Evidence from China,

2023,

120,

01409883,

106579,

10.1016/j.eneco.2023.106579

17.

Junshi Lan, Wenli Li, Xinwu Zhu,

The road to green development: How can carbon emission trading pilot policy contribute to carbon peak attainment and neutrality? Evidence from China,

2022,

13,

1664-1078,

10.3389/fpsyg.2022.962084

18.

Cong Wang, Pengyu Chen, Yuanyuan Hao, Abd Alwahed Dagestani,

Tax incentives and green innovation—The mediating role of financing constraints and the moderating role of subsidies,

2022,

10,

2296-665X,

10.3389/fenvs.2022.1067534

19.

Jiaying Peng, Yuhang Zheng,

Does Environmental Policy Promote Energy Efficiency? Evidence From China in the Context of Developing Green Finance,

2021,

9,

2296-665X,

10.3389/fenvs.2021.733349

20.

Jiaqi Chang, Xuhan Xu,

Network structure of urban digital financial technology and its impact on the risk of commercial banks,

2022,

30,

2688-1594,

4740,

10.3934/era.2022240

21.

Maomao Zhang, Shukui Tan, Zichun Pan, Daoqing Hao, Xuesong Zhang, Zhenhuan Chen,

The spatial spillover effect and nonlinear relationship analysis between land resource misallocation and environmental pollution: Evidence from China,

2022,

321,

03014797,

115873,

10.1016/j.jenvman.2022.115873

22.

Xiaoli Hao, Xinhui Wang, Haitao Wu, Yu Hao,

Path to sustainable development: Does digital economy matter in manufacturing green total factor productivity?,

2023,

31,

0968-0802,

360,

10.1002/sd.2397

23.

Xiaojie Huang, Gaoke Liao,

Identifying driving factors of urban digital financial network—based on machine learning methods,

2022,

30,

2688-1594,

4716,

10.3934/era.2022239

24.

Changjing Wei, Xuesen Cai, Xiaowei Song,

Towards achieving the sustainable development goal 9: Analyzing the role of green innovation culture on market performance of Chinese SMEs,

2023,

13,

1664-1078,

10.3389/fpsyg.2022.1018915

25.

Siying Yang, Dawei Feng, Jingjing Lu, Chuncao Wang,

The effect of venture capital on green innovation: Is environmental regulation an institutional guarantee?,

2022,

318,

03014797,

115641,

10.1016/j.jenvman.2022.115641

26.

Bohan Sun, Ruiqi Sun, Ke Gao, Yifan Zhang, Shuyue Wang, Puxian Bai,

Analyzing the mechanism among rural financing constraint mitigation, agricultural development, and carbon emissions in China: A sustainable development paradigm,

2022,

0958-305X,

0958305X2211434,

10.1177/0958305X221143413

27.

Xujun Liu, Jinzhe Chai, Yuanqing Luo, Shuqing Wang, Bei Liu,

How to achieve sustainable development: From the perspective of science and technology financial policy in China,

2022,

30,

1614-7499,

26078,

10.1007/s11356-022-23874-0

28.

Jiayi Li, Shujun Ye, Shujuan Wang,

Spatial Network Analysis on the Coupling Coordination of Digital Finance and Technological Innovation,

2023,

15,

2071-1050,

6354,

10.3390/su15086354

29.

Yanling Li, Mengxin Wang, Gaoke Liao, Ran Gu,

The impact of digital finance on energy total factor productivity,

2023,

36,

1331-677X,

10.1080/1331677X.2023.2263535

30.

Jianhua Sun, Shaobo Hou, Yuxia Deng, Huaicheng Li,

New media environment, green technological innovation and corporate productivity: Evidence from listed companies in China,

2024,

131,

01409883,

107395,

10.1016/j.eneco.2024.107395

31.

Ziyi Wang, Haolong Chen, Prasanna Divigalpitiya,

How does ICT development in resource-exhausted cities promote the urban green transformation efficiency? Evidence from China,

2024,

115,

22106707,

105835,

10.1016/j.scs.2024.105835

32.

Meng Yang, Hujun Li, Fangzhao Deng, Qinchen Yang, Ning Ba, Yunxia Guo, Haitao Wu, Muhammad Irfan, Yu Hao,

Inclusivity between internet development and energy conservation in Henan, China,

2023,

16,

1570-646X,

10.1007/s12053-023-10144-2

Mengxin Wang, Ran Gu, Meng Wang, Junru Zhang. Research on the impact of finance on promoting technological innovation based on the state-space model[J]. Green Finance, 2021, 3(2): 119-137. doi: 10.3934/GF.2021007

Mengxin Wang, Ran Gu, Meng Wang, Junru Zhang. Research on the impact of finance on promoting technological innovation based on the state-space model[J]. Green Finance, 2021, 3(2): 119-137. doi: 10.3934/GF.2021007

Note: The test forms (C, T, K) mean that the test equation includes constant term (C), time trend (T), and the order of the lag term. N means no C or T, respectively. △ is the difference operator.

Note: The figures in square brackets under the estimated coefficients are the corresponding Z-statistics. *, **, and *** indicate that the coefficient is significant at the significance level of 0.01, 0.05, and 0.10, respectively.

Enterprise Funds, Government Funds, Venture Capital Funds

Growth stage

Enterprise Funds, Government Funds, Venture Capital Funds, Loans from Financial Institutions, Capital Market Funds

Mature stage

Enterprise Funds, Loans from Financial Institutions, Capital Market Funds

Category

Indicators

Unit

Symbol

Symbol after the logarithm

Financial Methods

Enterprise Funds Government Funds Venture Capital Funds Loans from Financial Institutions Capital Market Funds

ten thousand yuan

X1 X2 X3 X4 X5

LX1 LX2 LX3 LX4 LX5

TI achievements

Number of R & D Projects Number of Patent Applications Sales Revenue of New Product

item item ten thousand yuan

Y1 Y2 Y3

LY1 LY2 LY3

Means

Min.

Max.

Standard deviation

Coefficient of variation

X1

1,345,606.12

295,861.76

3,134,186.90

896,009.26

0.6659

X2

30,665.01

3,592.08

68,903.27

20,489.58

0.6682

X3

190,981.52

12,224.85

1,655,287.60

435,929.45

2.2826

X4

13,181.05

2,440.89

31,851.85

9,072.55

0.6883

X5

261,441.23

10,290.55

692,546.03

225,298.84

0.8618

Y1

6,342.00

1,952.13

11,295.00

3,063.37

0.4830

Y2

6,977.44

847.87

16,707.00

5,360.66

0.7683

Y3

17,869,040.97

3,981,710.01

43,647,419.69

12,208,908.09

0.6832

Variables

Test form

ADF statistics

5% critical value

Stationarity

LX1

(C, N, 0)

−2.8239

−3.0810

No

△LX1

(C, T, 0)

−5.6778

−3.7912

Yes

LX2

(C, T, 0)

−1.6767

−3.7597

No

△LX2

(N, N, 0)

−2.9936

−1.9684

Yes

LX3

(C, N, 1)

−1.4562

−3.0989

No

△LX3

(N, N, 0)

−2.2677

−1.9684

Yes

LX4

(C, N, 1)

−2.3256

−3.0989

No

△LX4

(N, N, 0)

−2.1784

−1.9684

Yes

LX5

(C, N, 1)

−1.8031

−3.0989

No

△LX5

(C, N, 0)

−7.2057

−3.0989

Yes

LY1

(C, T, 0)

−2.4127

−3.7597

No

△LY1

(C, N, 3)

−2.8689

−2.7290*

Yes

LY2

(C, T, 0)

−2.0013

−3.7597

No

△LY2

(N, N, 0)

−3.7684

−1.9684

Yes

LY3

(C, N, 0)

−2.9483

−3.0810

Yes

Note: The test forms (C, T, K) mean that the test equation includes constant term (C), time trend (T), and the order of the lag term. N means no C or T, respectively. △ is the difference operator.

Variables

Hypothesised No. of CE(s)

Eigenvalue

Trace statistic

0.05 critical value

Prob.

LY1

None*

0.988848

140.6625

95.75366

0.0000

At most 1*

0.901636

73.21989

69.81889

0.0261

At most 2

0.812776

38.43371

47.85613

0.2834

LY2

None*

0.992396

140.2445

95.75366

0.0000

At most 1

0.834754

67.05821

69.81889

0.0814

LY3

None*

0.994823

146.1508

95.75366

0.0000

At most 1

0.871422

67.19824

69.81889

0.0795

Note: * indicates significance at the 5% level.

Parameter

LY1 (development stage)

LY2 (growth stage)

LY3 (maturity stage)

Initial model

Final model

Initial model

Final model

Initial model

Final model

Coefficient values

C(1)

2.3591(0.9317)

1.5878(0.7975)

−4.0103(−4.4421)*

−4.1364(−5.5004)*

3.4850(6.8625)*

3.7282(12.7510)*

C(2)

−3.7168(−10.4641)*

−3.8986(−9.8832)*

−5.0390(−8.1404)*

−4.9115(−8.5220)*

−5.4609(−6.7240)*

−5.6389(−13.4142)*

Final value of dynamic parameter

SV(1)

0.1875(1.4410)

0.2423(3.7790)*

0.5557(8.2735)*

0.6351(11.3461)*

0.9507(17.4790)*

0.9306(799.8982)*

SV(2)

0.3502(1.7952)**

0.3766(4.2495)*

0.3893(3.8652)*

0.3216(3.2761)*

0.0057(0.0697)

—

SV(3)

0.0156(0.3114)

—

0.0399(1.5460)

—

0.0225(1.0772)

—

SV(4)

−0.059674(−0.8305)

—

−0.1562(−4.2115)*

−0.1370(−3.6404)*

−0.0233(−0.7768)

—

SV(5)

0.054959(0.7202)

—

0.1773(4.4997)*

0.1732(4.1240)*

−0.0095(−0.2967)

—

Note: The figures in square brackets under the estimated coefficients are the corresponding Z-statistics. *, **, and *** indicate that the coefficient is significant at the significance level of 0.01, 0.05, and 0.10, respectively.

Year

Development stage

Growth stage

Mature stage

SV(1)

SV(2)

SV(1)

SV(2)

SV(4)

SV(5)

SV(1)

2005

0.3383

0.2395

0.3411

0.2414

0.2619

0.2441

0.9358

2006

0.4247

0.1175

0.3576

0.2098

0.2463

0.2692

0.9336

2007

0.3011

0.2814

0.3605

0.2520

0.1889

0.2849

0.9319

2008

0.2328

0.3882

0.3840

0.2052

−0.1010

0.2567

0.9327

2009

0.2178

0.4108

0.5130

0.5145

−0.1041

0.1285

0.9318

2010

0.2214

0.4051

0.5216

0.5090

−0.1074

0.1246

0.9301

2011

0.1993

0.4378

0.5150

0.5143

−0.1150

0.1357

0.9300

2012

0.1703

0.4805

0.5082

0.5038

−0.0979

0.1382

0.9303

2013

0.1731

0.4763

0.5066

0.5058

−0.1001

0.1406

0.9301

2014

0.1962

0.4429

0.5621

0.4267

−0.1103

0.1485

0.9301

2015

0.2214

0.4060

0.5739

0.4027

−0.1113

0.1555

0.9298

2016

0.2523

0.3616

0.6188

0.3683

−0.1339

0.1487

0.9295

2017

0.2422

0.3766

0.6158

0.3655

−0.1308

0.1525

0.9298

2018

0.2424

0.3766

0.6351

0.3216

−0.1370

0.1732

0.9306

Figure 1. Dynamic parameter chart of enterprise funds and government funds

Figure 2. Dynamic parameter charts in the growth stage

Figure 3. Dynamic parameter chart during the maturity period

Figure 4. Dynamic parameter charts of enterprise funds and government funds

Catalog

Abstract

1.

Introduction

2.

TI stages and financing methods

2.1. Stages of TI

2.2. Financing methods of TI

2.3. Financing methods in each stage

3.

Evaluation index system and model

3.1. Evaluation index system

3.2. Descriptive analysis of variables

3.3. Evaluation model

4.

Empirical test of the model

4.1. Stationarity and co-integration test

4.2. Empirical results of the model

5.

Analysis of results

5.1. Variable parameter analysis of the development stage

5.2. Variable parameter analysis of the growth stage

5.3. Variable parameter analysis of the mature stage

DownLoad:

DownLoad: