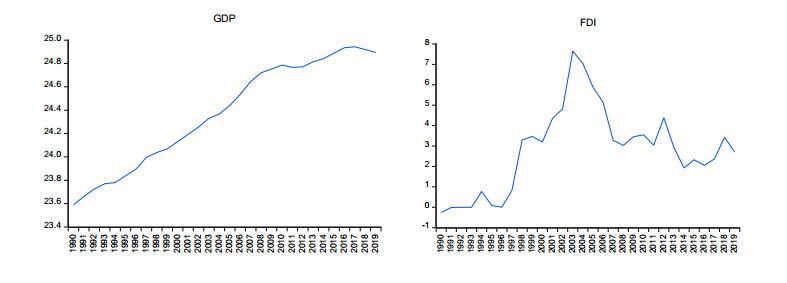

This study examined the nexus between foreign direct investment (FDI), financial development, and sustainable economic growth in Sudan during the period of the structural adjustment program and the full Islamization of the banking and financial system that took place in the 1980s. The research provides a comprehensive analysis using the most recent time series secondary data from 1990 to 2020 and the study employed co-integration, Granger causality, and VAR error correction technique to estimate the models, to clarify the claimed relationship between FDI and its effect on the financial sector and subsequently attending a sustainable economic development in Sudan. In this research, Augmented Dickey-Fuller (ADF) unit root tests are applied to test the stationarity of data and the data was found stationary at first difference. The results of the ARDL bounds showed the existence of a long-term relationship between the FDI and other independent variables but the short-term showed otherwise. The Granger causality test implies that the past values of FDI don't significantly contribute to the prediction of sustainable economic growth. Also, results show that there's evidence of observed causality running from the country's trade openness and the financial sector's development. The implication of these results shows there is a complementary relationship between sustainable economic growth and both financial development and trade openness in the short run. Interestingly, the findings of the study show that the effect of financial development on economic growth is further enhanced by the inflows of FDI.

Citation: Mustafa Hassan Mohammad Adam. Nexus among foreign direct investment, financial development, and sustainable economic growth: Empirical aspects from Sudan[J]. Quantitative Finance and Economics, 2022, 6(4): 640-657. doi: 10.3934/QFE.2022028

This study examined the nexus between foreign direct investment (FDI), financial development, and sustainable economic growth in Sudan during the period of the structural adjustment program and the full Islamization of the banking and financial system that took place in the 1980s. The research provides a comprehensive analysis using the most recent time series secondary data from 1990 to 2020 and the study employed co-integration, Granger causality, and VAR error correction technique to estimate the models, to clarify the claimed relationship between FDI and its effect on the financial sector and subsequently attending a sustainable economic development in Sudan. In this research, Augmented Dickey-Fuller (ADF) unit root tests are applied to test the stationarity of data and the data was found stationary at first difference. The results of the ARDL bounds showed the existence of a long-term relationship between the FDI and other independent variables but the short-term showed otherwise. The Granger causality test implies that the past values of FDI don't significantly contribute to the prediction of sustainable economic growth. Also, results show that there's evidence of observed causality running from the country's trade openness and the financial sector's development. The implication of these results shows there is a complementary relationship between sustainable economic growth and both financial development and trade openness in the short run. Interestingly, the findings of the study show that the effect of financial development on economic growth is further enhanced by the inflows of FDI.

| [1] | Abdalla OA, Mohamed AA, Abdelmawla MA, et al. (2015) Evaluation of foreign direct investment inflow in Sudan: An empirical investigation (1990–2013). J Bus Stud Quart 7: 149–168. |

| [2] | Abu N, Gobna WO, Usman A (2010) On the causal links between foreign direct investment and economic growth in Nigeria, 1970–2008: An application of Granger causality and co-integration techniques. Romanian Stat Rev 3: 57–76. |

| [3] |

Alfaro L, Chanda A, Kalemli-Ozcan S, et al. (2004) FDI and economic growth: the role of local financial markets. J Int Econ 64: 89–112. https://doi.org/10.1016/S0022-1996(03)00081-3 doi: 10.1016/S0022-1996(03)00081-3

|

| [4] |

Alfaro L, Chanda A, Kalemli-Ozcan S, et al. (2010) Does foreign direct investment promote growth? Exploring the role of financial markets on linkages. J Dev Econ 91: 242–256. https://doi.org/10.1016/j.jdeveco.2009.09.004 doi: 10.1016/j.jdeveco.2009.09.004

|

| [5] |

Akbas YE, Senturk M, Sancar C (2013) Testing for causality between the foreign direct investment, current account deficit, GDP and Total credit: Evidence from G7. Panoeconomicus 60: 791–812. http://dx.doi.org/10.2298/PAN1306791A doi: 10.2298/PAN1306791A

|

| [6] | Ali MAM (2018) Impact of foreign direct investment on domestic investment in Sudan: Giving Hope Hypothesis. J Econ Coop Dev 3: 39–64. |

| [7] | Aliber RZ (1970) A theory of foreign direct investment. International Cooperation MIT press. |

| [8] | Altaee HHA, Saied SM, Esmaeel ES, et al. (2014) Financial development, trade openness and economic growth: Evidence from Sultanate of Oman (1972–2012). J Econ Sustain Dev 5: 64–75. |

| [9] |

Asiedu E (2002) On the determinants of foreign direct investment to developing countries: Is Africa different? World Dev 30: 107–119. https://doi.org/10.1016/S0305-750X(01)00100-0 doi: 10.1016/S0305-750X(01)00100-0

|

| [10] |

Asteriou D, Moudatsou A (2014) FDI, finance, and growth: Further empirical evidence from a panel of 73 countries. Appl Econ Financ 1: 48–57. https://doi.org/10.11114/aef.v1i2.480 doi: 10.11114/aef.v1i2.480

|

| [11] | Barro RJ, Mankiw, NA, Sala-I-Martin X (1995) Capital mobility in neoclassical models of growth. Am Econ Rev 85: 103–115. |

| [12] |

Borensztein E, De Gregorio J, Lee JW (1998) How does foreign direct investment affect economic growth? J Int Econ 45: 115–135. https://doi.org/10.1016/S0022-1996(97)00033-0 doi: 10.1016/S0022-1996(97)00033-0

|

| [13] | Central Bank of Sudan (CBS) Economic and Financial Statistical Review data (various issues). Available from: https://cbos.gov.sd/en/periodicals-publications. |

| [14] |

Chakrabarti A (2001) The determinants of foreign direct investment: Sensitivity analysis of cross-country regression. Kyklos 54: 89–113. https://doi.org/10.1111/1467-6435.00142 doi: 10.1111/1467-6435.00142

|

| [15] |

Dankyi AB, Abban OJ, Yusheng K, et al. (2022) Human capital, foreign direct investment, and economic growth: Evidence from ECOWAS in a decomposed income level panel. Environ Chall 9: 1–13. https://doi.org/10.1016/j.envc.2022.100602 doi: 10.1016/j.envc.2022.100602

|

| [16] |

Dickey DA, Fuller WA (1981) Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 49: 1057–1072. https://doi.org/10.2307/1912517 doi: 10.2307/1912517

|

| [17] |

Engle RF, Granger CWJ (1987) Cointegration and Error Correction: Representation, Estimation, Testing. Econometrica 55: 1057–1072. https://doi.org/10.2307/1913236 doi: 10.2307/1913236

|

| [18] |

Findlay R (1978) Relative backwardness, foreign direct investment and the transfer of technology: A simple dynamic model. Quart J Econ 92: 1–16. http://dx.doi.org/10.2307/1885996 doi: 10.2307/1885996

|

| [19] |

Granger CWJ (1988) Some recent developments in a concept of causality. J Econ 39: 199–211. http://dx.doi.org/10.1016/0304-4076(88)90045-0 doi: 10.1016/0304-4076(88)90045-0

|

| [20] |

Gui-Diby SL (2014) Impact of foreign direct investments on economic growth in Africa: Evidence from three decades of panel data analyses. Res Econ 68: 248–256. https://doi.org/10.1016/j.rie.2014.04.003 doi: 10.1016/j.rie.2014.04.003

|

| [21] | Hussein MA (2009) Impacts of Foreign Direct Investment on Economic Growth in the Gulf Cooperation Council (GCC) Countries. Int Rev Bus Res Pap 5: 362–376. |

| [22] |

Hermes N, Lensink R (2003) Foreign Direct Investment, Financial Development, and Economic Growth. J Dev Stud 40: 142–163. https://doi.org/10.1080/00220380412331293707 doi: 10.1080/00220380412331293707

|

| [23] |

Ibrahim OA, Hassan HM (2013) Determinants of foreign direct investment in Sudan: an econometric perspective. J North Afric Stud 18: 1–15. http://dx.doi.org/10.1080/13629387.2012.702013 doi: 10.1080/13629387.2012.702013

|

| [24] |

Iamsiraroj S (2016) The foreign direct investment-economic growth nexus. Int Rev Econ Financ 42: 116–133. https://doi.org/10.1016/j.iref.2015.10.044 doi: 10.1016/j.iref.2015.10.044

|

| [25] |

Johansen S, Juselius K (1990) Maximum likelihood estimation and inferences on cointegration with application to the demand for money. Oxford B Econ Stat 52: 169–210. https://doi.org/10.1111/j.1468-0084.1990.mp52002003.x doi: 10.1111/j.1468-0084.1990.mp52002003.x

|

| [26] |

Lamine KM, Yang D (2010) Foreign direct investment effect on economic growth: Evidence from the Guinea Republic in West Africa. Int J Financ Res 1: 49–54. https://doi.org/10.5430/ijfr.v1n1p49 doi: 10.5430/ijfr.v1n1p49

|

| [27] |

Lutfi A, Ashraf M, Watto WA, et al. (2022) Do Uncertainty and Financial Development Influence the FDI Inflow of a Developing Nation? A Time Series ARDL Approach. Sustainability 14: 12609. https://doi.org/10.3390/su141912609 doi: 10.3390/su141912609

|

| [28] | Mohamed MA (2003) The impact of foreign capital inflow on savings, investment and economic growth rate in Egypt: An econometric analysis. Sci J King Faisal Univ 4: 279–308. |

| [29] |

Mohamed SE, Sidiropoulos MG (2010) Another look at the determinants of foreign direct investment in MENA countries: An empirical investigation. J Econ Dev 35: 75–95. http://dx.doi.org/10.35866/caujed.2010.35.2.005 doi: 10.35866/caujed.2010.35.2.005

|

| [30] |

Morina F, Grima S (2022) The impact of pension fund assets on economic growth in transition countries, emerging economies, and developed countries. Quant Financ Econ 6: 459–504. https://doi.org/10.3934/QFE.2022020 doi: 10.3934/QFE.2022020

|

| [31] |

Najid A, Hayat MF, Luqman M, et al. (2012) The causal links between Foreign Direct Investment and Economic Growth in Pakistan. Eur J Bus Econ 6: 20–21. https://doi.org/10.12955/ejbe.v6i0.137 doi: 10.12955/ejbe.v6i0.137

|

| [32] | Omankhanlen AE (2011) The effect of exchange rate and inflation on foreign direct investment and its relationship with economic growth in Nigeria. Annals of "Dunarea de Jos" University of Galati Fascicle I. Econ Appl Inform 1: 5–16. |

| [33] |

Omran M, Bolbol B (2003) Foreign direct investment, financial development, and economic growth: evidence from the Arab countries. Rev Middle East Econ Financ 1: 231–249. https://doi.org/10.2202/1475-3693.1014 doi: 10.2202/1475-3693.1014

|

| [34] |

Osabuohien-Irabor O, Drapkin IM (2022) FDI Escapism: the effect of home country risks on outbound investment in the global economy. Quant Financ Econ 6: 113–138. https://doi.org/10.3934/QFE.2022005 doi: 10.3934/QFE.2022005

|

| [35] |

Pesaran MH, Shin Y, Smith JR (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16: 289–326. https://doi.org/10.1002/jae.616 doi: 10.1002/jae.616

|

| [36] |

Philips PCB, Perron P (1988) Testing for a unit root in time series regressions. Biometrika 75: 335–346. https://doi.org/10.2307/2336182 doi: 10.2307/2336182

|

| [37] |

Pradhan RP (2010) Financial deepening, foreign direct investment, and economic growth: Are they cointegrated. Int J Financ Res 1: b37–b43. https://doi.org/10.5430/ijfr.v1n1p37 doi: 10.5430/ijfr.v1n1p37

|

| [38] |

Qamruzzaman Md, Wei J (2019) Do financial inclusion, stock market development attract foreign capital flows in developing economy: a panel data investigation. Quant Financ Econ 3: 88–108. https://doi.org/10.3934/QFE.2019.1.88 doi: 10.3934/QFE.2019.1.88

|

| [39] | Saibu MO, Nwosa IP, Agbeluyi AM (2011) Financial deepening, foreign direct investment and economic growth in Nigeria. J Emerg Trends Econ Manag Sci 2: 146–154. https://journals.co.za/doi/10.10520/EJC133886 |

| [40] |

Sarker B, Farid K (2020) Nexus Between Foreign Direct Investment and Economic Growth in Bangladesh: An Augmented Autoregressive Distributed Lag Bounds Testing Approach. Financ Innov 6: 10. https://doi.org/10.1186/s40854-019-0164-y doi: 10.1186/s40854-019-0164-y

|

| [41] | Sghaier IM, Abida Z (2013) Foreign direct investment, financial development, and economic growth: Empirical evidence from North African countries. J Int Glob Econ Stud 6: 1–13 |

| [42] |

Sirag A, SidAhmed S, Ali HS (2018) Financial development, FDI and economic growth: evidence from Sudan. Int J Soc Econ 45: 1236–1249. https://doi.org/10.1108/IJSE-10-2017-0476 doi: 10.1108/IJSE-10-2017-0476

|

| [43] |

Sjöholm F (1999) Technology gap, competition, and spillovers from foreign direct investment: Evidence from establishment data. J Dev Stud 36: 53–73. https://doi.org/10.1080/00220389908422611 doi: 10.1080/00220389908422611

|

| [44] |

Tanaya O, Suyanto S (2022) The causal nexus between foreign direct investment and economic growth in Indonesia: An autoregressive distributed lag bounds testing approach. Period Polytech Soc Manage Sci 30: 57–69. https://doi.org/10.3311/PPso.16799 doi: 10.3311/PPso.16799

|

| [45] | UNCTAD (2003) World Investment Report 2003—FDI Policies for Development: National and International Perspectives. |

| [46] | UNCTAD (2014) World Investment Report 2008 Data. Available from: https://unctadstat.unctad.org/EN/. |

| [47] |

Wang JY, Blomström M (1992) Foreign investment and technology transfer: A simple model. Eur Econ Rev 36: 137–155. https://doi.org/10.1016/0014-2921(92)90021-N doi: 10.1016/0014-2921(92)90021-N

|

| [48] | World Bank (2021) World Development Indicators. Washington, D.C: World Bank. Available from: https://datatopics.worldbank.org/world-development-indicators. |

| [49] |

Yahia YE, Haiyun L, Khan MA, et al. (2018) The impact of foreign direct investment on domestic investment: Evidence from Sudan. Intl J Econ Financ Iss 8: 1–10. https://doi.org/10.32479/ijefi.6895 doi: 10.32479/ijefi.6895

|

| [50] |

Yanikkaya H (2003) Trade openness and economic growth: a cross-country empirical investigation. J Dev Econ 72: 57–89. https://doi.org/10.1016/S0304-3878(03)00068-3 doi: 10.1016/S0304-3878(03)00068-3

|

| [51] | Zakaria Z (2007) The causality relationship between financial development and foreign direct investment. Jurnal Kemanusiaan 14: 1–23. |

Figures(1) / Tables(7)

Mustafa Hassan Mohammad Adam. Nexus among foreign direct investment, financial development, and sustainable economic growth: Empirical aspects from Sudan[J]. Quantitative Finance and Economics, 2022, 6(4): 640-657. doi: 10.3934/QFE.2022028

DownLoad:

DownLoad: