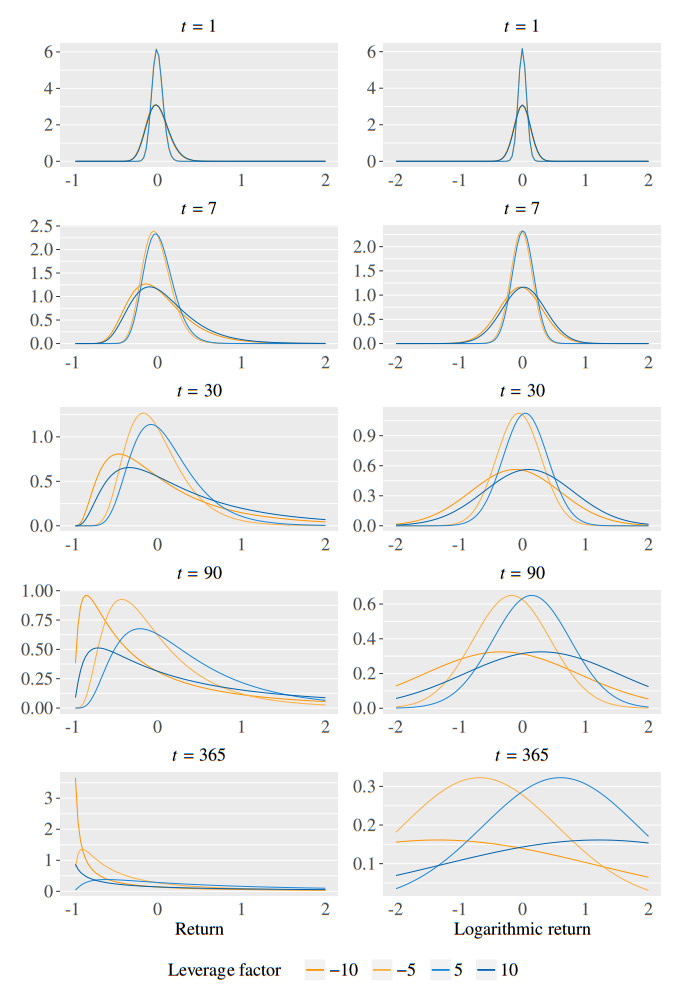

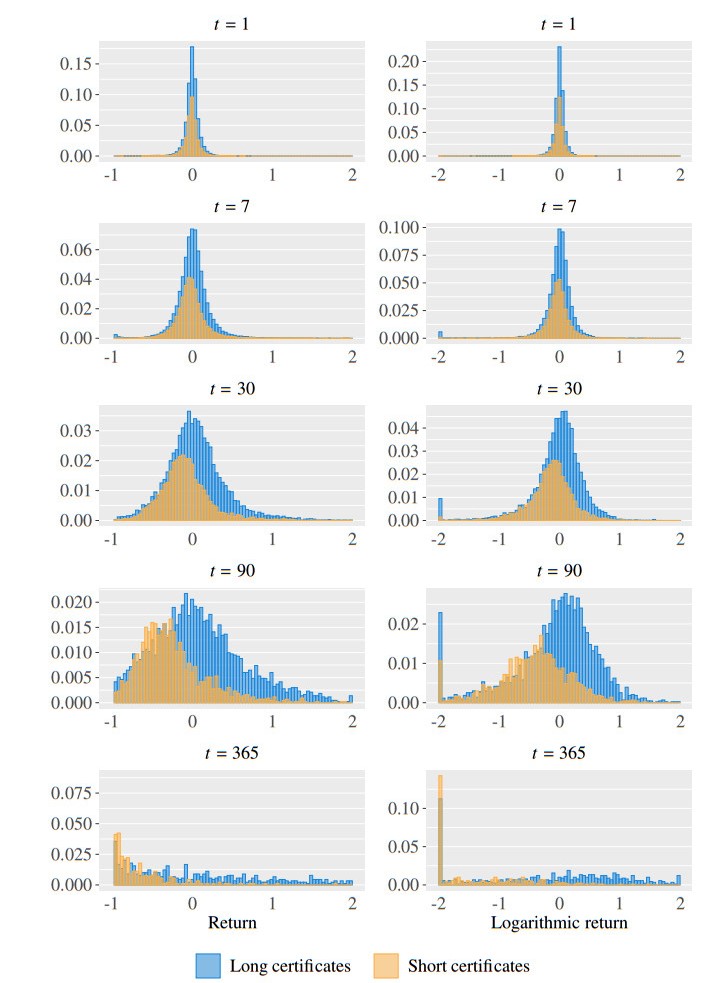

This paper analyzes a relatively new investment product named as constant leverage certificate (CLC), which is designed to provide a multiple of the return of its underlying asset on a daily basis. Based on the literature on leveraged ETFs, which have a similar design, it is well-known that such a strategy does not reproduce the corresponding multiple of the underlying in the long run. But due to the typically much larger leverage factors of CLCs compared to leveraged ETFs, it is questionable whether many of the results found for leveraged ETFs can be applied to these certificates as well. Against this background, I study the drivers of the long-term deviation of the product return from the leveraged return of the underlying, test a generalized version of the theoretical long-term return model originally developed for leveraged ETFs with a simulation study, and analyze the return distribution based on the theoretical model and empirical data. In contrast to prior literature, my results indicate that the effect of compounding is much more pronounced than the noncompounding deviation also for short-term investment periods. The theoretical model, however, is relatively accurate despite much larger leverage factors.

Citation: Vladimir Anic. 2020: Constant leverage certificates: dynamics, performance, and risk-return characteristics, Quantitative Finance and Economics, 4(4): 693-724. doi: 10.3934/QFE.2020032

This paper analyzes a relatively new investment product named as constant leverage certificate (CLC), which is designed to provide a multiple of the return of its underlying asset on a daily basis. Based on the literature on leveraged ETFs, which have a similar design, it is well-known that such a strategy does not reproduce the corresponding multiple of the underlying in the long run. But due to the typically much larger leverage factors of CLCs compared to leveraged ETFs, it is questionable whether many of the results found for leveraged ETFs can be applied to these certificates as well. Against this background, I study the drivers of the long-term deviation of the product return from the leveraged return of the underlying, test a generalized version of the theoretical long-term return model originally developed for leveraged ETFs with a simulation study, and analyze the return distribution based on the theoretical model and empirical data. In contrast to prior literature, my results indicate that the effect of compounding is much more pronounced than the noncompounding deviation also for short-term investment periods. The theoretical model, however, is relatively accurate despite much larger leverage factors.

| [1] | Andersen TG, Bollerslev T (1998) Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. Int Econ Rev 39: 885-905. |

| [2] | Avellaneda M, Zhang S (2010) Path-dependence of leveraged ETF returns. SIAM J Financ Math 1:586-603. |

| [3] | Bansal VK, Marshall JF (2015) A tracking error approach to leveraged ETFs: Are they really that bad? Global Financ J 26: 47-63. |

| [4] | Charupat N, Miu P (2011) The pricing and performance of leveraged exchange-traded funds. J Bank Financ 35: 966-977. |

| [5] | Chen JH, Diaz JF (2012) Spillover and asymmetric-volatility effects of leveraged and inverse leveraged exchange traded funds. J Bus Policy Res 7: 1-10. |

| [6] | Engle R (2001) GARCH 101: The use of ARCH/GARCH models in applied econometrics. J Econ Perspect 15: 157-168. |

| [7] | Entrop O, Scholz H, Wilkens M (2009) The price-setting behavior of banks: An analysis of open-end leverage certificates on the German market. J Bank Financ 33: 874-882. |

| [8] | Eusipa (2019) Eusipa Market Report on Structured Investment Products. Available from: https://eusipa.org/wp-content/uploads/EUSIPA-Q3-2019-market-report_final.pdf. |

| [9] | Giannetti A (2017) The dynamics of leveraged ETFs returns: a panel data study. Quant Financ 17:745-761. |

| [10] | Giese G (2010) On the risk-return profile of leveraged and inverse ETFs. J Asset Manage 11: 219-228. |

| [11] | Hansen PR, Lunde A (2005) A forecast comparison of volatility models: Does anything beat a GARCH (1, 1)? J Appl Econometrics 20: 873-889. |

| [12] | Harčariková M, Bobriková M (2019) Leverage certificates' design within the portfolio management. Scientific papers of the University of Pardubice, Series D, Faculty of Economics and Administration, 45/2019. |

| [13] | Jarrow RA (2010) Understanding the risk of leveraged ETFs. Financ Res Lett 7: 135-139. |

| [14] | Koopman SJ, Jungbacker B, Hol E (2005) Forecasting daily variability of the S & P 100 stock index using historical, realised and implied volatility measurements. J Empirical Financ 12: 445-475. |

| [15] | Loviscek A, Tang H, Xu XE (2014) Do leveraged exchange-traded products deliver their stated multiples? J Bank Financ 43: 29-47. |

| [16] | Lu L, Wang J, Zhang G (2009) Long term performance of leveraged ETFs. Financ Serv Rev 21: 63-80. |

| [17] | Murphy R, Wright C (2010) An empirical investigation of the performance of commodity-based leveraged ETFs. J Index Investing 1: 14-23. |

| [18] | Rossetto S, Van Bommel J (2009) Endless leverage certificates. J Bank Financ 33: 1543-1553. |

| [19] | Ruf T (2011) The dynamics of overpricing in structured products. Available at SSRN 1787216. |

| [20] | Sabbatini M, Linton O (1998) A GARCH model of the implied volatility of the Swiss market index from option prices. Int J Forecast 14: 199-213. |

| [21] | Smirnov M, Smirnov A (2020) Robust Leveraged ETF Portfolios Extending Classic 40/60 Portfolios and Portfolio Insurance. Available at SSRN 3549581. |

| [22] | Stoimenov PA, Wilkens S (2005) Are structured products 'fairly' priced? An analysis of the German market for equity-linked instruments. J Bank Financ 29: 2971-2993. |

| [23] | Tang H, Xu XE (2013) Solving the return deviation conundrum of leveraged exchange-traded funds. J Financ Quant Anal 48: 309-342. |

| [24] | Trainor W (2011) Daily vs. monthly rebalanced leveraged funds. J Financ Accountancy 6: 1-14. |

| [25] | Wilkens S, Erner C, Röder K (2003) The pricing of structured products in Germany. J Derivatives 11:55-69. |

QFE2020165-Supplementary.zip QFE2020165-Supplementary.zip |

|

Figures(6) / Tables(4)

Vladimir Anic. 2020: Constant leverage certificates: dynamics, performance, and risk-return characteristics, Quantitative Finance and Economics, 4(4): 693-724. doi: 10.3934/QFE.2020032

DownLoad:

DownLoad: