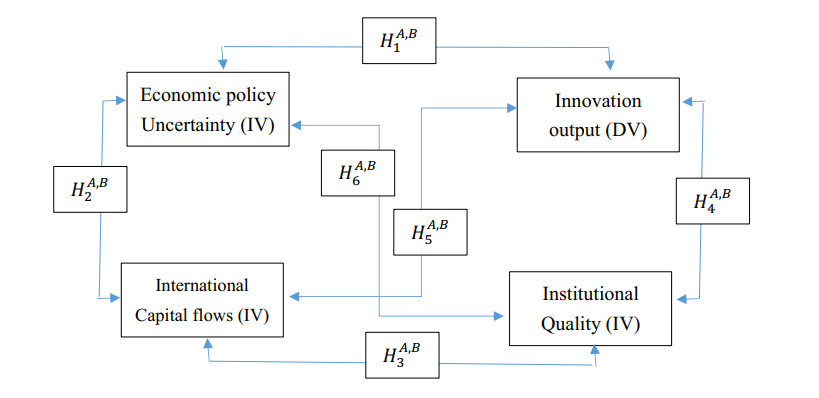

The determinants of innovation output in empirical literature have been extensively investigated by considering diverse sets of variables. Still, the impact of economic policy uncertainty on innovation output is yet to unleash. The study investigates the association between EPU and innovation output to mitigate the existing research gap, considering a panel of 22 countries over 1997–2018. The study employs a dynamic panel quantile regression and system-GMM specification causality test to discover elasticity and directional association both in the long and short run. Study findings disclosed negative statistically significant effects running from EPU to innovation output except innovation measured by R & D.; moreover, institutional quality and FDI expose positive and statistically significant association with innovation output. In directional causality, unidirectional causality runs from EPU and FDI to innovation output, whereas bidirectional causality establishes between institutional quality and innovation output.

Citation: Md Qamruzzaman. Do international capital flows, institutional quality matter for innovation output: the mediating role of economic policy uncertainty[J]. Green Finance, 2021, 3(3): 351-382. doi: 10.3934/GF.2021018

The determinants of innovation output in empirical literature have been extensively investigated by considering diverse sets of variables. Still, the impact of economic policy uncertainty on innovation output is yet to unleash. The study investigates the association between EPU and innovation output to mitigate the existing research gap, considering a panel of 22 countries over 1997–2018. The study employs a dynamic panel quantile regression and system-GMM specification causality test to discover elasticity and directional association both in the long and short run. Study findings disclosed negative statistically significant effects running from EPU to innovation output except innovation measured by R & D.; moreover, institutional quality and FDI expose positive and statistically significant association with innovation output. In directional causality, unidirectional causality runs from EPU and FDI to innovation output, whereas bidirectional causality establishes between institutional quality and innovation output.

| [1] | Aghion P, Van Reenen J, Zingales L (2009) Innovation andInstitutional Ownership. NBER Working Paper 14769. |

| [2] |

Aizenman J, Spiegel MM (2006) Institutional efficiency, monitoring costs and the investment share of FDI. Rev Int Econ 14: 683-697. doi: 10.1111/j.1467-9396.2006.00595.x

|

| [3] | Akram R, Chen F, Khalid F, et al. (2020) Heterogeneous effects of energy efficiency and renewable energy on carbon emissions: Evidence from developing countries. J Clean Prod 247: 119122. |

| [4] | Aldieri L, Barra C, Ruggiero N, et al. (2020) Innovative performance effects of institutional quality: an empirical investigation from the Triad. Appl Econ, 1-13. |

| [5] |

Alesina A, Perotti R (1996) Income distribution, political instability, and investment. Eur Econ Rev 40: 1203-1228. doi: 10.1016/0014-2921(95)00030-5

|

| [6] |

Andrijauskiene M, Dumčiuvienė D (2019) Inward Foreign Direct Investment and National Innovative Capacity. Eng Econ 30: 339-348. doi: 10.5755/j01.ee.30.3.22832

|

| [7] |

Anokhin S, Schulze WS (2009) Entrepreneurship, innovation, and corruption. J Bus Ventur 24: 465-476. doi: 10.1016/j.jbusvent.2008.06.001

|

| [8] |

Antonakakis N, Cunado J, Filis G, et al. (2017) Oil dependence, quality of political institutions and economic growth: A panel VAR approach. Resour Policy 53: 147-163. doi: 10.1016/j.resourpol.2017.06.005

|

| [9] | Arellano M (2003) Panel data econometrics, Oxford university press. |

| [10] |

Arellano M, Bond S (1991) Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev Econ Stud 58: 277-297. doi: 10.2307/2297968

|

| [11] |

Arellano M, Bover O (1995) Another look at the instrumental variable estimation of error-components models. J Econometrics 68: 29-51. doi: 10.1016/0304-4076(94)01642-D

|

| [12] |

Arun K, Yıldırım DÇ (2017) Effects of foreign direct investment on intellectual property, patents and R & D. Queen Mary J Intell Property 7: 226-241. doi: 10.4337/qmjip.2017.02.05

|

| [13] |

Asamoah ME, Adjasi CK, Alhassan AL (2016) Macroeconomic uncertainty, foreign direct investment and institutional quality: Evidence from Sub-Saharan Africa. Econ Syst 40: 612-621. doi: 10.1016/j.ecosys.2016.02.010

|

| [14] | Asiedu E (2013) Foreign direct investment, natural resources and institutions. Int Growth Centre. |

| [15] | Baltagi B (2008a) Econometric analysis of panel data, John Wiley & Sons. |

| [16] |

Baltagi BH (2008b) Forecasting with panel data. J Forecasting 27: 153-173. doi: 10.1002/for.1047

|

| [17] |

Baum CF, Schaffer ME, Stillman S (2007) Enhanced routines for instrumental variables/generalized method of moments estimation and testing. Stata J 7: 465-506. doi: 10.1177/1536867X0800700402

|

| [18] |

Berger M, Diez JR (2008) Can host innovation systems in late industrializing countries benefit from the presence of transnational corporations? Insights from Thailand's manufacturing industry. Eur Plann Stud 16: 1047-1074. doi: 10.1080/09654310802315708

|

| [19] | Bertschek I (1995) Product and process innovation as a response to increasing imports and foreign direct investment. J Ind Econ, 341-357. |

| [20] |

Blind K, Jungmittag A (2004) Foreign direct investment, imports and innovations in the service industry. Rev Ind Organ 25: 205-227. doi: 10.1007/s11151-004-3537-x

|

| [21] | Blomström M, Kokko A (1998) Foreign investment as a vehicle for international technology transfer. Creation Transfer Knowl, 279-311. |

| [22] |

Bloom N (2014) Fluctuations in uncertainty. J Econ Perspect 28: 153-176. doi: 10.1257/jep.28.2.153

|

| [23] |

Bloom N, Bond S, Van Reenen J (2007) Uncertainty and investment dynamics. Rev Econ Stud 74: 391-415. doi: 10.1111/j.1467-937X.2007.00426.x

|

| [24] |

Blundell R, Bond S (1998) Initial conditions and moment restrictions in dynamic panel data models. J Econometrics 87: 115-143. doi: 10.1016/S0304-4076(98)00009-8

|

| [25] | Borensztein E, De Gregorio J, Lee JW (1998) How does foreign direct investment affect economic growth? J Int Econ 45: 115-135. |

| [26] | Bosworth D (2009) The R & D, knowledge, innovation triangle: education and economic performance, Review for the Beyond Current Horizons Programme. Bristol: Futurelab. Available from: www. beyondcurrenthorizons. org. uk/evidence/work-and-employment. |

| [27] |

Breusch TS, Pagan AR (1980) The Lagrange multiplier test and its applications to model specification in econometrics. Rev Econ Stud 47: 239-253. doi: 10.2307/2297111

|

| [28] | Brunello G, Garibaldi P, Wasmer E (2007) Higher education, innovation and growth, In: Education Training In Europe, Oxford University Press. |

| [29] |

Buchanan BG, Le QV, Rishi M (2012) Foreign direct investment and institutional quality: Some empirical evidence. Int Rev Financ Anal 21: 81-89. doi: 10.1016/j.irfa.2011.10.001

|

| [30] |

Canh NP, Schinckus C, Thanh SD (2019) Do economic openness and institutional quality influence patents? Evidence from GMM systems estimates. Int Econ 157: 134-169. doi: 10.1016/j.inteco.2018.10.002

|

| [31] | Carlin W, Soskice D (2008) Reforms, macroeconomic policy and economic performance in Germany, Econ Policy Proposals Germany Europe, Routledge, 82-128. |

| [32] | Chen Y (2007) Impact of foreign direct investment on regional innovation capability: a case of China. J Data Sci 5: 577-596. |

| [33] |

Chen Y, Puttitanun T (2005) Intellectual property rights and innovation in developing countries. J Dev Econ 78: 474-493. doi: 10.1016/j.jdeveco.2004.11.005

|

| [34] |

Cheng C, Ren X, Wang Z, et al. (2019) Heterogeneous impacts of renewable energy and environmental patents on CO2 emission-Evidence from the BRIICS. Sci Total Environ 668: 1328-1338. doi: 10.1016/j.scitotenv.2019.02.063

|

| [35] |

Cheung KY, Ping L (2004) Spillover effects of FDI on innovation in China: Evidence from the provincial data. China Econ Rev 15: 25-44. doi: 10.1016/S1043-951X(03)00027-0

|

| [36] | Clarke G (2001) How the quality of institutions affects technological deepening in developing countries, The World Bank. |

| [37] | Coluccia D, Dabić M, Del Giudice M, et al. (2019) R & D innovation indicator and its effects on the market. An empirical assessment from a financial perspective. J Bus Res 119: 259-271. |

| [38] |

Combes JL, Ebeke C (2011) Remittances and household consumption instability in developing countries. World Dev 39: 1076-1089. doi: 10.1016/j.worlddev.2010.10.006

|

| [39] |

Crafts N (2006) Regulation and productivity performance. Oxford Rev Econ Policy 22: 186-202. doi: 10.1093/oxrep/grj012

|

| [40] |

Crescenzi R, Rodriguez-Pose A, Storper M (2007) The territorial dynamics of innovation: a Europe-United States comparative analysis. J Econ Geogr 7: 673-709. doi: 10.1093/jeg/lbm030

|

| [41] |

Dakhli M, De Clercq D (2004) Human capital, social capital, and innovation: a multi-country study. Entrep Reg Dev 16: 107-128. doi: 10.1080/08985620410001677835

|

| [42] | Daude C, Stein E (2007) The quality of institutions and foreign direct investment. EconPolitics 19: 317-344. |

| [43] |

Dincer O (2019) Does corruption slow down innovation? Evidence from a cointegrated panel of US states. European J Political Econ 56: 1-10. doi: 10.1016/j.ejpoleco.2018.06.001

|

| [44] | Dotta V, Munyo I (2019) Trade Openness and Innovation. Innovation J 24: 1-13. |

| [45] | Dutta S, Lanvin B, Wunsch-Vincent S (2018) Global innovation index 2018: Energizing the world with innovation. WIPO. |

| [46] |

Ervits I, Zmuda M (2018) A cross-country comparison of the effects of institutions on internationally oriented innovation. J Int Entrepreneurship 16: 486-503. doi: 10.1007/s10843-018-0225-8

|

| [47] | Fang C, Mohnen P (2010) FDI, R & D and Innovation Output in the Chinese Automobile Industry, In: Fu X., Soete L. (eds), The Rise of Technological Power in the South, Palgrave Macmillan, London, 203-220. |

| [48] |

Farole T, Rodríguez‐Pose A, Storper M (2011) Cohesion policy in the European Union: growth, geography, institutions. J Common Market Stud 49: 1089-1111. doi: 10.1111/j.1468-5965.2010.02161.x

|

| [49] | Filippetti A, Frenz M, Ietto-Gillies G (2017) The impact of internationalization on innovation at countries' level: the role of absorptive capacity. Cambridge J Econ 41: 413-439. |

| [50] |

Gani A (2007) Governance and foreign direct investment links: evidence from panel data estimations. Appl Econ Lett 14: 753-756. doi: 10.1080/13504850600592598

|

| [51] | GAO SX, XU X, LI YH (2010) Empirical Study on the Impact of Technology Spillover of FDI on the Innovation Output of Chinese Enterprises. J Ind Eng Eng Manage 2. |

| [52] |

Gholipour HF (2019) The effects of economic policy and political uncertainties on economic activities. Res Int Bus Financ 48: 210-218. doi: 10.1016/j.ribaf.2019.01.004

|

| [53] |

Girma S, Gong Y, Gö rg H (2008) Foreign direct investment, access to finance, and innovation activity in Chinese enterprises. World Bank Econ Rev 22: 367-382. doi: 10.1093/wber/lhn009

|

| [54] |

Globerman S, Shapiro D (2002) Global foreign direct investment flows: The role of governance infrastructure. World Dev 30: 1899-1919. doi: 10.1016/S0305-750X(02)00110-9

|

| [55] |

Gradstein M (2004) Governance and growth. J Dev Econ 73: 505-518. doi: 10.1016/j.jdeveco.2003.05.002

|

| [56] | Gulen H, Ion M (2016) Policy uncertainty and corporate investment. Rev Financ Stud 29: 523-564. |

| [57] |

Habib M, Zurawicki L (2002) Corruption and foreign direct investment. J Int Bus Stud 33: 291-307. doi: 10.1057/palgrave.jibs.8491017

|

| [58] |

Hall BH (2002) The financing of research and development. Oxford Rev Econ Policy 18: 35-51. doi: 10.1093/oxrep/18.1.35

|

| [59] |

Han C, Phillips PC, Sul D (2014) X-differencing and dynamic panel model estimation. Econometric Theory 30: 201-251. doi: 10.1017/S0266466613000170

|

| [60] |

Hartono A, Kusumawardhani R (2019) Innovation barriers and their impact on innovation: Evidence from Indonesian manufacturing firms. Global Bus Rev 20: 1196-1213. doi: 10.1177/0972150918801647

|

| [61] |

Hsu PH, Tian X, Xu Y (2014) Financial development and innovation: Cross-country evidence. J Financ Econ 112: 116-135. doi: 10.1016/j.jfineco.2013.12.002

|

| [62] |

Huang Y, Zhang Y (2020) The innovation spillovers from outward and inward foreign direct investment: a firm-level spatial analysis. Spatial Econ Anal 15: 43-59. doi: 10.1080/17421772.2019.1618484

|

| [63] | Huang Y, Zhu H, Zhang Z (2020) The heterogeneous effect of driving factors on carbon emission intensity in the Chinese transport sector: Evidence from dynamic panel quantile regression. Sci Total Environ 727: 138578. |

| [64] |

Huang H, Xu C (1999) Institutions, innovations, and growth. Am Econ Rev 89: 438-443. doi: 10.1257/aer.89.2.438

|

| [65] |

Im KS, Pesaran MH, Shin Y (2003) Testing for unit roots in heterogeneous panels. J Econometrics 115: 53-74. doi: 10.1016/S0304-4076(03)00092-7

|

| [66] | Islam MA, Liu H, Khan MA, et al. (2018) Causal relationship between economic growth, financial deepening, foreign direct investment and innovation: Evidence from China. Asian Econ Financ Rev 8: 1086. |

| [67] | Jacob S (1966) Invention and economic growth, J. Schmookler. Cambridge Mass: Harvard University Press. |

| [68] | Janoskova K, Kral P (2019) An in-depth analysis of the summary innovation index in the V4 countries. J Competitiveness 11: 68. |

| [69] | Jian LPCXL (2007) Performance Analysis of R & D Capital Input and Output in Chinese Independent Innovation: with Discussion of the Effects of Human Capital and Intellectual Property Rights Protection. Social Sci China 2: 32-42. |

| [70] |

Julio B, Yook Y (2012) Political uncertainty and corporate investment cycles. J Financ 67: 45-83. doi: 10.1111/j.1540-6261.2011.01707.x

|

| [71] | Kacani J (2020) Innovation as a Prerequisite for Trade Openness in Emerging Economies, In: A Data-Centric Approach to Breaking the FDI Trap Through Integration in Global Value Chains, 267-285. |

| [72] |

Kang W, Perez de Gracia F, Ratti RA (2017) Oil price shocks, policy uncertainty, and stock returns of oil and gas corporations. J Int Money Financ 70: 344-359. doi: 10.1016/j.jimonfin.2016.10.003

|

| [73] |

Kao C (1999) Spurious regression and residual-based tests for cointegration in panel data. J Econometrics 90: 1-44. doi: 10.1016/S0304-4076(98)00023-2

|

| [74] |

Karnizova L, Li JC (2014) Economic policy uncertainty, financial markets and probability of US recessions. Econ Lett 125: 261-265. doi: 10.1016/j.econlet.2014.09.018

|

| [75] | Kaufmann D, Kraay A, Mastruzzi M (2010) Governance indicators for 2000-2008, the worldwide governance indicators (WGI) project. World Bank Policy Res. |

| [76] |

Khachoo Q, Sharma R (2016) FDI and innovation: An investigation into intra-and inter-industry effects. Global Econ Rev 45: 311-330. doi: 10.1080/1226508X.2016.1218294

|

| [77] | Kinoshita Y (1998) Technology spillovers through foreign direct investment. CERGE-EI Working Paper Series. |

| [78] | Kiselakova D, Sofrankova B, Onuferova E, et al. (2020) Assessing the effect of innovation determinants on macroeconomic development within the EU (28) countries. Probl Perspect Manage 18: 277. |

| [79] | Knott AM, Vieregger C (2018) Reconciling the firm size and innovation puzzle. US Census Bureau Center for Economic Studies Paper No. CES-WP-16-20. |

| [80] | Koçak E (2017) Does institutional quality drive innovation? Evidence from system-GMM estimates. 1367-1374. |

| [81] |

Koenker R (2004) Quantile regression for longitudinal data. J Multivar Anal 91: 74-89. doi: 10.1016/j.jmva.2004.05.006

|

| [82] |

Kotha R, Zheng Y, George G (2011) Entry into new niches: The effects of firm age and the expansion of technological capabilities on innovative output and impact. Strat Manage J 32: 1011-1024. doi: 10.1002/smj.915

|

| [83] |

Kraft H, Schwartz E, Weiss F (2018) Growth options and firm valuation. Eur Financ Manage 24: 209-238. doi: 10.1111/eufm.12141

|

| [84] |

Kwan LYY, Chiu CY (2015) Country variations in different innovation outputs: The interactive effect of institutional support and human capital. J Organ Behav 36: 1050-1070. doi: 10.1002/job.2017

|

| [85] |

Law SH, Sarmidi T, Goh LT (2020) Impact of innovation on economic growth: Evidence from Malaysia. Malays J Econ Stud 57: 113-132. doi: 10.22452/MJES.vol57no1.6

|

| [86] |

Law SH, Tan HB, Azman-Saini W (2014) Financial development and income inequality at different levels of institutional quality. Emerg Mark Financ Trade 50: 21-33. doi: 10.2753/REE1540-496X5001S102

|

| [87] |

Le TH, Kim J, Lee M (2016) Institutional quality, trade openness, and financial sector development in Asia: An empirical investigation. Emerg Mark Financ Trade 52: 1047-1059. doi: 10.1080/1540496X.2015.1103138

|

| [88] |

Lee S, Nam Y, Lee S, et al. (2016) Determinants of ICT innovations: A cross-country empirical study. Technol Forecasting Social Change 110: 71-77. doi: 10.1016/j.techfore.2015.11.010

|

| [89] | Leoncini R (2017) 13 Innovation and inequality. Inequality Econ Sociology New Perspectives: 189. |

| [90] |

Levchenko AA (2007) Institutional quality and international trade. Rev Econ Stud 74: 791-819. doi: 10.1111/j.1467-937X.2007.00435.x

|

| [91] |

Levin A, Lin CF, Chu CSJ (2002) Unit root tests in panel data: asymptotic and finite-sample properties. J Econometrics 108: 1-24. doi: 10.1016/S0304-4076(01)00098-7

|

| [92] |

Li J, Strange R, Ning L, et al. (2016) Outward foreign direct investment and domestic innovation performance: Evidence from China. Int Bus Rev 25: 1010-1019. doi: 10.1016/j.ibusrev.2016.01.008

|

| [93] |

Li Q, Resnick A (2003) Reversal of fortunes: Democratic institutions and foreign direct investment inflows to developing countries. Int organ 57: 175-211. doi: 10.1017/S0020818303571077

|

| [94] | Loukil K (2016) Foreign direct investment and technological innovation in developing countries. Oradea J Bus Econ 1: 31-40. |

| [95] | Malik S (2020) Macroeconomic Determinants of Innovation: Evidence from Asian Countries. Global Bus Rev, 0972150919885494. |

| [96] | Maradana RP, Pradhan RP, Dash S, et al. (2017) Does innovation promote economic growth? Evidence from European countries. J Innovation Entrepreneurship 6: 1. |

| [97] |

Marcelin I, Mathur I (2014) Financial development, institutions and banks. Int Rev Financ Anal 31: 25-33. doi: 10.1016/j.irfa.2013.09.003

|

| [98] | Masso J, Reino A, Varblane U (2010) Foreign direct investment and innovation in Central and Eastern Europe: Evidence from Estonia. The University of Tartu Faculty of Economics and Business Administration Working Paper. |

| [99] |

Masso J, Roolaht T, Varblane U (2013) Foreign direct investment and innovation in Estonia. Baltic J Manage 8: 231-248. doi: 10.1108/17465261311310036

|

| [100] | Meierrieks D (2014) Financial development and innovation: Is there evidence of a Schumpeterian finance-innovation nexus? Annals Econ Financ 15: 61-81. |

| [101] | Nelson RR, Peck MJ, Kalachek ED (1967) Technology, economic growth, and public policy; a Rand Corporation and Brookings Institution study. |

| [102] | Nyeadi JD, Adjasi C (2020) Foreign direct investment and firm innovation in selected sub-Saharan African Countries. Cogent Bus Manage 7: 1763650. |

| [103] |

Oltra MJ, Flor M (2003) The impact of technological opportunities and innovative capabilities on firms' output innovation. Creativity Innovation Manage 12: 137-144. doi: 10.1111/1467-8691.00277

|

| [104] |

Pan X, Uddin MK, Han C, et al. (2019) Dynamics of financial development, trade openness, technological innovation and energy intensity: Evidence from Bangladesh. Energy 171: 456-464. doi: 10.1016/j.energy.2018.12.200

|

| [105] |

Pedroni P (1999) Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bull Econ Stat 61: 653-670. doi: 10.1111/1468-0084.61.s1.14

|

| [106] |

Pedroni P. (2001) Purchasing power parity tests in cointegrated panels. Rev Econ Stat 83: 727-731. doi: 10.1162/003465301753237803

|

| [107] | Pedroni P (2004) Panel cointegration: asymptotic and finite sample properties of pooled time series tests with an application to the PPP hypothesis. Econ Theory 20: 597-625. |

| [108] | Pesaran MH (2004) General diagnostic tests for cross section dependence in panels. |

| [109] |

Pesaran MH (2006) Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica 74: 967-1012. doi: 10.1111/j.1468-0262.2006.00692.x

|

| [110] |

Pesaran MH (2007) A simple panel unit root test in the presence of cross‐section dependence. J Appl Econometrics 22: 265-312. doi: 10.1002/jae.951

|

| [111] |

Pesaran MH, Ullah A, Yamagata T (2008) A bias‐adjusted LM test of error cross‐section independence. Econometrics J 11: 105-127. doi: 10.1111/j.1368-423X.2007.00227.x

|

| [112] |

Pesaran MH, Yamagata T (2008) Testing slope homogeneity in large panels. J Econometrics 142: 50-93. doi: 10.1016/j.jeconom.2007.05.010

|

| [113] | Poelhekke S, van der Ploeg R (2010) Do natural resources attract FDI? Evidence from non-stationary sector level data. |

| [114] |

Qamruzzaman M, Jianguo W (2020) The asymmetric relationship between financial development, trade openness, foreign capital flows, and renewable energy consumption: Fresh evidence from panel NARDL investigation. Renew Energy 159: 827-842. doi: 10.1016/j.renene.2020.06.069

|

| [115] |

Rodríguez-Pose A, Di Cataldo M (2015) Quality of government and innovative performance in the regions of Europe. J Econ Geogr 15: 673-706. doi: 10.1093/jeg/lbu023

|

| [116] | Romer PM (1990) Endogenous technological change. J Political Econ 98: S71-S102. |

| [117] | Sala-i-Martin X (2001) Comment on'growth empirics and reality, by William A. Brock and Steven N. Durlauf. |

| [118] | Sattar A, Mahmood T (2011) Intellectual property rights and Economic growth: Evidences from high, middle and low income countries. Pakistan Econ Social Rev, 163-186. |

| [119] | Schumpeter JA (2013) Capitalism, socialism and democracy, routledge. |

| [120] |

Shabani ZD, Shahnazi R (2019) Energy consumption, carbon dioxide emissions, information and communications technology, and gross domestic product in Iranian economic sectors: a panel causality analysis. Energy 169: 1064-1078. doi: 10.1016/j.energy.2018.11.062

|

| [121] |

Sivalogathasan V, Wu X. (2014) The effect of foreign direct investment on innovation in south Asian emerging markets. Global Bus Organ Excellence 33: 63-76. doi: 10.1002/joe.21544

|

| [122] |

Solow RM (1956) A contribution to the theory of economic growth. Q J Econ 70: 65-94. doi: 10.2307/1884513

|

| [123] | Solow RM (1957) Technical change and the aggregate production function. Rev Econ Stat, 312-320. |

| [124] | Soto M (2009) System GMM estimation with a small sample. |

| [125] | Stiebale J, Reize F (2008) The impact of FDI on innovation in target firms. Ruhr Econ Paper. |

| [126] | Sudolska A, Łapińska J (2020) Exploring Determinants of Innovation Capability in Manufacturing Companies Operating in Poland. Sustainability 12: 7101. |

| [127] | Tajaddini R, Gholipour HF (2020) Economic policy uncertainty, R & D expenditures and innovation outputs. J Econ Stud. |

| [128] |

Tebaldi E, Elmslie B (2013) Does institutional quality impact innovation? Evidence from cross-country patent grant data. Appl Econ 45: 887-900. doi: 10.1080/00036846.2011.613777

|

| [129] | Ustalar SA, Şanlisoy S (2016) The Impact of Foreign Direct Investment on Innovation Performance: Evidence from a Nonlinear ARDL Approach. İzmir J Econ 35: 77-89. |

| [130] |

Van Vo L, Le HTT (2017) Strategic growth option, uncertainty, and R & D investment. Int Rev Financ Anal 51: 16-24. doi: 10.1016/j.irfa.2017.03.002

|

| [131] |

Varsakelis NC (2006) Education, political institutions and innovative activity: A cross-country empirical investigation. Res Policy 35: 1083-1090. doi: 10.1016/j.respol.2006.06.002

|

| [132] | Villalba E (2007) The relationship between education and innovation. Evidence from European indicators. Available from: crell. jrc. ec. europa. eu/Publications/.../EUR22797_EDandINN. pdf 1. |

| [133] | Villanueva ACB (2019) Does Institutional Quality Affect Firm Performance? Evidence From The Philippines, Indonesia And Viet Nam. |

| [134] | Wang C, Qiao C, Ahmed RI, et al. (2020) Institutional Quality, Bank Finance and Technological Innovation: A way forward for Fourth Industrial Revolution in BRICS Economies. Technol Forecasting Social Change, 120427. |

| [135] |

Wang CC, Wu A (2016) Geographical FDI knowledge spillover and innovation of indigenous firms in China. Int Bus Rev 25: 895-906. doi: 10.1016/j.ibusrev.2015.12.004

|

| [136] |

Westerlund J (2007) Testing for error correction in panel data. Oxford Bull Econ Stat 69: 709-748. doi: 10.1111/j.1468-0084.2007.00477.x

|

| [137] | Wignaraja G (2008) FDI and Innovation as Drivers of Export Behaviour: Firm-level Evidence from East Asia. UNU-MERIT Working Paper. |

| [138] |

Wijeweera A, Dollery B (2009) Host country corruption level and Foreign Direct Investments inflows. Int J Trade Global Mark 2: 168-178. doi: 10.1504/IJTGM.2009.025387

|

| [139] |

Wong PK, Ho YP, Autio E (2005) Entrepreneurship, innovation and economic growth: Evidence from GEM data. Small Bus Econ 24: 335-350. doi: 10.1007/s11187-005-2000-1

|

| [140] | Wu H, Ren S, Xie G (2020) Technology Import and China's Innovation Capability: Does Institutional Quality Matter? Region Econ Dev Res, 93-104. |

| [141] |

Wu J, Ma Z, Zhuo S (2017) Enhancing national innovative capacity: The impact of high-tech international trade and inward foreign direct investment. Int Bus Rev 26: 502-514. doi: 10.1016/j.ibusrev.2016.11.001

|

| [142] | Wusiman N, Ndzembanteh AN (2020) The Impact of Human Capital and Innovation Output on Economic Growth: Comparative Analysis of Malaysia and Turkey. Anemon Muş Alparslan Ü niversitesi Sosyal Bilimler Dergisi 8: 231-242. |

| [143] | Yilun M (2020) The Influence of Foreign Direct Investment on China's High-tech Industry Innovation—A Mediation Effect Model. Int J Sci Eng Sci 4: 15-18. |

| [144] |

Zhang YJ, Peng HR, Liu Z, et al. (2015) Direct energy rebound effect for road passenger transport in China: a dynamic panel quantile regression approach. Energy Policy 87: 303-313. doi: 10.1016/j.enpol.2015.09.022

|

| [145] |

Zhu H, Duan L, Guo Y, et al. (2016) The effects of FDI, economic growth and energy consumption on carbon emissions in ASEAN-5: evidence from panel quantile regression. Econ Model 58: 237-248. doi: 10.1016/j.econmod.2016.05.003

|

| [146] | Zhu X, Asimakopoulos S, Kim J (2020) Financial development and innovation-led growth: Is too much finance better? J Int Money Financ 100: 102083. |

Figures(1) / Tables(14)

Md Qamruzzaman. Do international capital flows, institutional quality matter for innovation output: the mediating role of economic policy uncertainty[J]. Green Finance, 2021, 3(3): 351-382. doi: 10.3934/GF.2021018

DownLoad:

DownLoad: