Citation: Didier Sornette, Peter Cauwels, Georgi Smilyanov. Can we use volatility to diagnose financial bubbles? lessons from 40 historical bubbles[J]. Quantitative Finance and Economics, 2018, 2(1): 486-590. doi: 10.3934/QFE.2018.1.1

| [1] | Abreu D, Brunnermeier MK (2003) Bubbles and crashes. Econome 71: 173-204. |

| [2] | Ahmed E, Rosser BJ, Uppal JY (2010) Emerging Markets and Stock Market Bubbles: Nonlinear Speculation? Emerg Mark Financ Tr 46: 23-40. |

| [3] | Allen F, Gale D (2000) Bubbles and crises. Econ J, 110:236-255. |

| [4] | Allen F, Gale D (2007) Understanding Financial Crises. Oxford University Press, New York. |

| [5] | Allen F, Morris S, Postlewaite A (1993) Finite bubbles with short sale constraints and asymmetric information. J Econ Theory 61: 206-229. |

| [6] | Andersen JV, Sornette D (2004) Fearless versus fearful speculative financial bubbles. Physica A, 337: 565-585. |

| [7] | Anderson K, Brooks C, Katsaris A (2013) Testing for speculative bubbles in asset prices. In A. R. Bell, C. Brooks and M. Prokopczuk, eds, Handb Research Methods Applica Empiri Financ. |

| [8] | Barro RJ, Fama EF, Fischel DR, et al. (1989) Black monday and the future of financial markets. Dow Jones-Irwin. |

| [9] | Barsky R (2009) The Japanese Bubble: A 'Heterogeneous' Approach. Technical Report 15052, NBER Working Paper. |

| [10] | Bastiaensen K, Cauwels P, Sornette D, et al. (2009) The Chinese Equity Bubble: Ready to Burst. Available from: http://arXiv.org/abs/0907.1827. |

| [11] | Bates DS (1991) The crash of '87: was it expected? the evidence from options markets. J Financ 46: 1009-1044. |

| [12] | Bates DS (2000) Post-'87 crash fears in the s & p 500 futures option market. J Econometrics 94: 181-238. |

| [13] | Baur DG, Glover K (2012) A Gold Bubble? Technical Report No 175, UTC Business SchoolWorking Paper. |

| [14] | Bear Markets since 1929, as defined by the S & P 500. Available from: http://www.feesonly.com/ClientLetterArchive/BearMarketsSince1929.pdf. |

| [15] | Bloomberg News, Palladium Crashes With Car Sales as Ratio Signals Bear Trade. URL http://www.bloomberg.com/news/2010-05-09/palladium-crashes-with-china-car-sales-as-platinum-trades-give-bear-signal.html. |

| [16] | Bloomberg News, Soros Sees Gold Prices on Brink of Bear Market. URL http://www.bloomberg.com/news/2011-12-29/\gold-bubble-seen-by-soros-ends-bull-year-on-bear-market-brink-commodities.html. |

| [17] | Bortolotti B, Beltratti A, Caccavaio M (2011) The Stock Market Reaction to the 2005 non-Tradable Share Reform in China. Working Paper 3: 583-590. |

| [18] | Beran J (1994) Statistics for Long-Memory Processes. Chapman & Hall/CRC, 1 edition. |

| [19] | Bergsten CF (1997). The Asian Monetary Crisis: Proposed Remedies. Statement before the Committee on Banking and Financial Services, US House of Representatives, November 13, Washington DC. |

| [20] | Bertrand KZ, Lagi M, Bar-Yam Y (2011) The Food Crises and Political Instability in North Africa and the Middle East. Soc Science Electron Publ. Available from: https://arXiv.org/pdf/1108.2455.pdf. |

| [21] | Bhattacharya U, Yu XY (2008) The causes and consequences of recent financial bubbles: an introduction. Rev Financ Stud 21: 3-10. |

| [22] | Blanchard O, Watson M (1982) Bubbles, rational expectations, and financial markets. In P. Wachter (ed. ), Cris Econ Financ Structure, Lexington, MA: Lexington Books: 295-315. |

| [23] | BIS. Total credit to the non-financial sector, 2017. Available from: https://www.bis.org/statistics/totcredit.htm. |

| [24] | Blustein P (2005) And the Money Kept Rolling In (And Out). Public Affairs. |

| [25] | Bohl MT, Siklos PL, Werner T (2007) Do Central Banks React to the Stock Market? The Case of the Bundesbank. J Bank Financ 31: 719-733. |

| [26] | Bouchaud J-P, Matacz A, PottersM(2001) Leverage effect in financial markets: The retarded volatility model. Phys Rev Lett 87: 228701. |

| [27] | Business Insider. Sugar Crash, 2010. Available from: http://www.businessinsider.com/sugar-crash-2010-11. |

| [28] | Brunnermeier MK, Oehmke M (2013) Bubbles, Financial Crises, and Systemic Risk. Handb Econ Financ 2: 1221-1288. |

| [29] | Calvet LE, Fisher AJ (2004) How to forecast long-run volatility: Regime switching and the estimation of multifractal processes. J Fin Econom 2: 49-83. |

| [30] | Camerer C (1989) Bubbles and fads in asset prices. J Econ Surv 3: 3-14. |

| [31] | Caputo R, Saravia D (2014) The Fiscal and Monetary History of Chile 1960-2010. Central Bank Chile. |

| [32] | Carlson M (2006) A Brief History of the 1987 Stock Market Crash with a Discussion of the Federal Reserve Response. Soc Science Electron Publ 2007-13. |

| [33] | Cauwels P (2017) Economic Ideas You Should Forget, chapter Chapter: Volatility Is Risk 33-34. |

| [34] | Colombo J (2012) Japan's bubble economy of the 1980s. Forbes column. |

| [35] | Corsi F, Sornette D (2014) Follow the money: The monetary roots of bubbles and crashes. Int Rev Financ Anal 32: 47-59. |

| [36] | Craig BR, Glatzer E, Keller J, et al. (2003) The Forecasting Performance of German Stock Option Densities. Technical Report 03-12, FRB of Cleveland Working Paper. |

| [37] | De Long JB, Shleifer A, Summers LH, et al. (1990) Noise trader risk in financial markets. J polit Econ 98: 703-738. |

| [38] | De Schutter Olivier (2010) Food Commodities Speculation and Food Price Crises. Technical report, United Nations Special Rapporteur on the Right to Food. |

| [39] | Diba B, Grossman H (1988) Explosive rational bubbles in stock prices? Am Econ Rev 78: 520-530. |

| [40] | Eckaus RS (2008) The Oil Price Really Is A Speculative Bubble. Technical report, MIT Center for Energy and Environmental Policy Research Working Paper. |

| [41] | ETF Database, SGG Tumbles: Historic Day For Sugar ETF, 2010. Available from: http://etfdb.com/2010/sgg-tumbles-historic-day-for-sugar-etf/. |

| [42] | Evanoff DD, Kaufman G, Malliaris AG (2012) New perspectives on asset price bubbles. Oxford University Press. |

| [43] | Evans G (1991) Pitfalls in testing for explosive bubbles in asset prices. Am Econ Rev 31: 922-930. |

| [44] | Figlewski S, Wang XZ (2000) Is the 'leverage effect' a leverage effect? Available at SSRN: http://ssrn.com/abstract=256109. |

| [45] | Filimonov VA, Sornette D (2011) Self-excited multifractal dynamics. Europhys Lett 94: 46003. |

| [46] | Financial Times. Swiss franc soars in hunt for haven, 2011. Available from: http://www.ft.com/cms/s/0/17df8456-c2ca-11e0-8cc7-00144feabdc0.html#axzz2N41WtKTy. |

| [47] | Flood R, Hodrick R, Kaplan P (1994) An evaluation of recent evidence on stock price bubbles. In R. Flood and P. Garber (eds. ), Speculative Bubbles, Speculative Attacks, and Policy Switching, Cambridge, MA: MIT Press: 105-133. |

| [48] | Flowerdew J (1998) The Final Years of British Hong Kong: The Discourse of Colonial Withdrawal. St. Martin's Press. |

| [49] | Forró Z, Woodard R, Sornette D (2015) Using trading strategies to detect phase transitions in financial markets. Phys Rev E 91: 042803. |

| [50] | Froot K, Obstfeld M (1991) Intrinsic bubbles: the case of stock prices. Am Econ Rev 81: 1189-1214. |

| [51] | Galbraith JK (2009) The Great Crash, 1929. Houghton Miffin Haircourt. |

| [52] | Greenspan A, Kennedy J (2005) Estimates of home mortgage originations, repayments, and debt on one-to-four-family residences. Finance and Economic Discussion Series, Washington Board of Governors of the Federal Reserve System, 2005-41. |

| [53] | Greenspan A, Kennedy K (2007) Sources and uses of equity extracted from homes. Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs, Federal Reserve Board, Washington, D. C. , 2007-20,2007. |

| [54] | Gürkaynak R (2008) Econometric tests of asset price bubbles: taking stock. J Econ Surv 22: 166-186. |

| [55] | Hamao Y, Mei J, Xu Y (2003) Idiosyncratic Risk and the Creative Destruction in Japan. Technical Report 9642, NBER Working Paper. |

| [56] | Hardouvelis GA (1988) Evidence on stock market speculative bubbles: Japan, the united states, and great britain. Federal Reserve Bank of New York Quarterly Review 13: 4-16. |

| [57] | Harrison M, Kreps DM (1978) Speculative investor behavior in a stock-market with heterogeneous expectations. Q J Econ 92: 323-336. |

| [58] | Homm, Breitung J (2012) Testing for speculative bubbles in stock markets: A comparison of alternative methods. J Financ Economet 10: 198-231. |

| [59] | Hong H, Stein JC (2003) Differences of opinion, short?sales constraints, and market crashes. Rev Financ Stud 16: 487-525. |

| [60] | Hong Kong Monetary Authority, Asset Pricing and Central Bank Policies: The Case of Hong Kong, 1997. Available from: http://www.hkma.gov.hk/eng/publications-and-research/quarterlybulletin/1998/may/qbfa03e.shtml. |

| [61] | Hüsler A, Sornette D, Hommes CH (2013) Super-exponential bubbles in lab experiments: evidence for anchoring over-optimistic expectations on price. J Econ Behav Organ 92: 304-316. |

| [62] | IMF Independent Evaluation Office, The IMF and Recent Capital Account Crises: Indonesia, Korea, Brazil, 2003. Technical report, IMF Evaluation Report. |

| [63] | Jao YC (2001) The Asian financial crisis and the ordeal of Hong Kong. Quorum Books, Westport, Connecticut, London. |

| [64] | Jarrow R, Kchia Y, Protter P (2011a) How to detect an asset bubble. SIAM J Financ Math 2: 839-865. |

| [65] | Jarrow R, Kchia Y, Protter P (2011b) Is There a Bubble in LinkedIn's Stock Price? J Portfolio Manage 38: 125-130. |

| [66] | Jarrow R, Protter P, Shimbo K (2006) Asset price bubbles in a complete market. Adv Math Financ 105-130. |

| [67] | Jarrow R, Protter P, Shimbo K (2010) Asset price bubbles in incomplete markets. Math Financ 20: 145-185. |

| [68] | Jiang ZQ, Zhou W-X, Sornette D, et al. (2010) Bubble Diagnosis and Prediction of the 2005-2007 and 2008-2009 Chinese stock market bubbles. J Econ Behav Organ 74: 149-162. |

| [69] | Johansen A, Ledoit O, Sornette D (2000) Crashes as critical points. Int J Theor Appl Financ 3: 219-255. |

| [70] | Johansen A, Sornette D (1999) Financial "anti-bubbles": log-periodicity in gold and nikkei collapses. Int J Mod Phys C 10: 563-575. |

| [71] | Johansen A, Sornette D (2000a) Evaluation of the quantitative prediction of a trend reversal on the japanese stock market in 1999. Int J Mod Phys C 11: 359-364. |

| [72] | Johansen A, Sornette D (2000b) The Nasdaq crash of April 2000: Yet another example of logperiodicity in a speculative bubble ending in a crash. Eur Phys J B 17: 319-328. |

| [73] | Johansen A, Sornette D (2001) Bubbles and anti-bubbles in Latin-American, Asian and Western stock markets: An empirical study. Int J Theor Appl Financ 4: 853-920. |

| [74] | Johansen A, Sornette D (2010) Shocks, Crashes and Bubbles in Financial Markets. Bruss Econ Rev 53: 201-253. |

| [75] | Johansen A, Sornette D, Ledoit O (1999) Predicting financial crashes using discrete scale invariance. J Risk 1: 5-32. |

| [76] | Jord O, Chularick M, Taylor AM (2015) Leveraged Bubbles. Technical report, Federal Reserve Bank of San Francisco Working Paper Series. URL http://www.frbsf.org/economic-research/files/wp2015-10.pdf. |

| [77] | Kaizoji T, Leiss M, Saichev A, et al. (2015) Super-exponential endogenous bubbles in an equilibrium model of rational and noise traders. J Econ Behav Organ 112: 289-310. |

| [78] | Kaizoji T, Sornette D (2010) Market Bubbles and Crashes. Encyclopedia Quant Financ (Wiley). Available from: http://arXiv.org/abs/0812.2449. |

| [79] | Kaufman GG, Hunter WC, PomerleanoM(2002) Asset Price Bubbles: The Implications for Monetary, Regulatory, and International Policies, chapter Chapter 3: Tropical Bubbles: Asset Price Bubbles in Latin America 1980-2001. |

| [80] | Khan MS (2009)The 2008 Oil Price "Bubble". Technical report, Peterson Institute for International Economics. Available from: http://www.iie.com/publications/pb/pb09-19.pdf. |

| [81] | Kindleberger C (1978) Manias, Panics, and Crashes: A History of Financial Crises. John Wiley & Sons, New York. |

| [82] | Kindleberger CP, Aliber RZ (2005) Manias, Panics, and Crashes: A History of Financial Crises. John Wiley & Sons, New York. |

| [83] | Koning JP (2004) Explaining the 1987 Stock Market Crash and Potential Implications. Available from: http://www.lope.ca/markets/1987crash/1987crash.pdf. |

| [84] | Kotz DM (1999) Russia's Financial Crisis: The Failure of Neoliberalism? Z Magazine 28-32. |

| [85] | Krugman P (1998) What happened to asia? http://web.mit.edu/krugman/www/disinter.html. |

| [86] | Lammerding M, Stephan P, Trede M, et al. (2013) Speculative bubbles in recent oil price dynamics: Evidence from a Bayesian Markov-switching state-space approach. Energy Econ 36: 491-502. |

| [87] | Leiss M, Nax HH, Sornette D (2015) Super-Exponential Growth Expectations and the Global Financial Crisis. J Econ Dyn Control 55: 1-13. |

| [88] | Lera S, Sornette D (2016) Quantitative modelling of the EUR/CHF exchange rate during the target zone regime of September 2011 to January 2015. J Int Money Financ 63: 28-47. |

| [89] | LeRoy S, Porter R (1981) The present-value relation: tests based on implied variance bounds. Econome 49: 555-574. |

| [90] | Lleo B, Ziemba WT (2012) Stock market crashes in 2007-2009: were we able to predict them? Quant Financ 12: 1161-1187. |

| [91] | Ma Y, Kanas A (2004) Intrinsic bubbles revisited: evidence from nonlinear cointegration and forecasting. J Forecasting 23: 237-250. |

| [92] | Magazine T (2009) Why China's Stock Market Bubble Is Fizzling. URL http://www.time.com/time/world/article/0,8599,1919777,00.html. |

| [93] | Malkiel AG, Urrutia JL (1992) The international crash of october 1987: Causality tests. J Financ Quant Anal 27: 353-364. |

| [94] | Malkiel BG (2007) A Random Walk Down Wall Street. W. W. Norton & Company. |

| [95] | Manoel D, Martin L (2004) Identification of Rational Speculative Bubbles in IBOVESPA (after the Real Plan) using Markov Switching Regimes. EconomiA, Selecta, Brasilia 5. |

| [96] | Minsky HP (1993) The Financial Stability Hypothesis. InHandb Radic Political Econ, P. Arestis and M. C. Saw-yer. Edward Elgar: Aldershot. |

| [97] | Musacchio A (2012) Mexico's Financial Crisis of 1994-1995. Technical Report 12-101, Harvard Business School Working Paper. |

| [98] | Nagel S, Brunnermeier MK (2004) Hedge funds and the technology bubble. J Financ 59: 2013-2040. |

| [99] | Nam CW (2008) What happened to Korea ten years ago? CESifo Forum 4: 69-73. |

| [100] | Neu CR, Lowell J, Tong D (1998) Financial Crises and Contagion in Emerging Market Countries. Technical report, RAND National Security Research Division. |

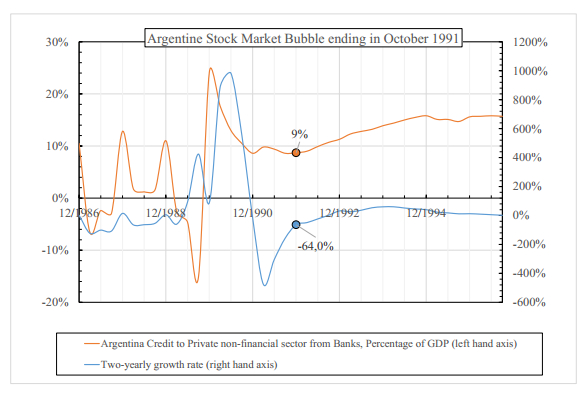

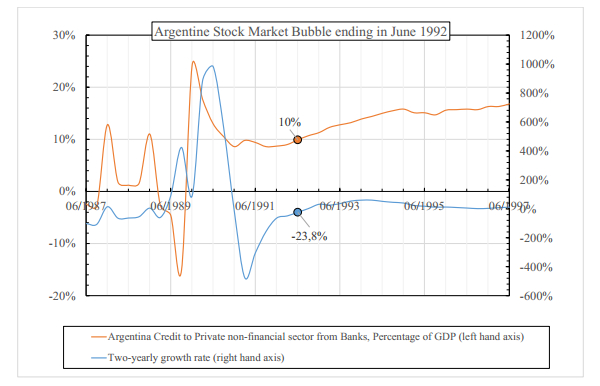

| [101] | Nochteff H (1996) The Argentine experience: development or a succession of bubbles. CEPRL Rev 59: 111-126. |

| [102] | Orléan A (1995) Bayesian interactions and collective dynamics of opinion -herd behavior and mimetic contagion. J Econ Behav Organ 28: 257-274. |

| [103] | Perry GE, Lederman D (1998) Financial Vulnerability, Spillover Effects, and Contagion: Lessons from the Asian Crises for Latin America. Technical report, World Bank Latin American and Caribbean Studies Viewpoints. |

| [104] | Phillips P, Wu Y, Yu J (2011) Explosive behavior in the 1990s Nasdaq: When did exuberance escalate asset values? Int Econ Rev 201: 201-226. |

| [105] | Phillips PCB, Shi SP, Yu J (2013) Testing for multiple bubbles: Historical Episodes of Exuberance and Collapse in the S & P 500. Int Econ Rev 56: 1043-1078. |

| [106] | Pinto B, Ulatov S (2010) Financial globalization and the russian crisis of 1998. The World Bank, Europe and Central Asia Region & The Managing Director? Office, Policy Research Working Paper 5312: 1-39. |

| [107] | Darst DM (2013) Portfolio Investment Opportunities in Precious Metals. Jpn J Pediatr Dent 40: 32-45. |

| [108] | Protter P (2013) A mathematical theory of financial bubbles. Lect Notes Math 2081: 1-108. |

| [109] | Rangel GJ, Pillay SS (2007) Evidence of bubbles in the Malaysian stock market. In Asia-Pac Financ Mark: Integr, Innov Chall. |

| [110] | Sang WK, Rogers JH (1995) International stock price spillovers and market liberalization: evidence from korea, japan and the united states. Int Financ Discuss Papers 2: 117-133. |

| [111] | Sato K (1995) Bubbles in Japan's Stock Market: A Macroeconomic Analysis. Jpn Econ 23: 32-58. |

| [112] | Scheffer M, Carpenter SR, Lenton TM, et al. (2012) Anticipating critical transitions. Science 338: 344-348. |

| [113] | Scheinkman JA, Xiong W (2003) Overconfidence and speculative bubbles. J Polit Econ 111: 1183-1219. |

| [114] | Scherbina A, Schlusche B (2014) Asset price bubbles: a survey. Quant Financ 14: 589-604. |

| [115] | Shiller R (1979) The volatility of long term interest rates and expectations models of the term structure. J Polit Econ 87: 1190-1209. |

| [116] | Shiller R (1981) Do stock prices move too much to be justified by subsequent changes in dividends? Am Econ Rev 71: 421-436. |

| [117] | Shiller RJ (2006) Irrational exuberance. Crown Business, 2nd edition. |

| [118] | Shiller RJ (2014) Speculative Asset Prices. Am Econ Rev 104: 1486-1517. |

| [119] | Shu-jie Y, Dan L (2008) Chinese Stock Market Bubble: Inevitable or Accidental? J Xi'an Jiaotong University(Soc Sci) 6. |

| [120] | Sornette D (2000) Stock Market Speculation: Spontaneous Symmetry Breaking of Economic Valuation. Phys A 284: 355-375. |

| [121] | Sornette D (2004) Critical Phenomena in Natural Sciences (Chaos, Fractals, Self-organization and Disorder: Concepts and Tools). Springer 37: 9604-9605. |

| [122] | Sornette D (2007) Keynote address on why stock markets crash?. Thurday 18 October 2007 at the Drobny global conference, Stockholm, Sweden, October 18-20. |

| [123] | Sornette D (2017) Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press (new print with new preface). |

| [124] | Sornette D, Andersen JV (2002) A nonlinear super-exponential rational model of speculative financial bubbles. Int J Mod Phys C 13: 171-188. |

| [125] | Sornette D, Cauwels P (2014) 1980-2008: The Illusion of the Perpetual Money Machine and what it bodes for the future. Risks 2: 103-131. |

| [126] | Sornette D, Cauwels P (2015a) Managing risk in a creepy world. J Risk Manage Financ Inst 83-108. |

| [127] | Sornette D, Cauwels P (2015b) Financial bubbles: mechanisms and diagnostics. Rev Behav Econ 2: 279-305. |

| [128] | Sornette D, Demos G, Zhang Q, et al. (2015) Real-time prediction and post-mortem analysis of the shanghai 2015 stock market bubble and crash. J Invest Strateg 4: 77-95. |

| [129] | Sornette D, Johansen A (2001) Significance of log-periodic precursors to financial crashes. Quant Financ 1: 452-471. |

| [130] | Sornette D, Johansen A, Bouchaud JP (1996) Stock market crashes, precursors and replicas. J Phys I France 6: 167-175. |

| [131] | Sornette D, von der Becke S. Crashes and high frequency trading (an evaluation of risks posed by high-speed algorithmic trading). report for the UK Government project entitled "The Future of Computer Trading in Financial Markets", Foresight Driver Review -DR7, Government Office for Science, 2nd Floor, 1 Victoria Street, London SW1H 0ET, United Kingdom, 2011 (http://ssrn.com/abstract=1976249). |

| [132] | Sornette D, Woodard R, Fedorovsky M (2011) The Financial Bubble Experiment: Advanced Diagnostics and Forecasts of Bubble Terminations Volume Ⅲ-Master Document. Available from: http://arXiv.org/abs/1011.2882. |

| [133] | Sornette D, Woodard R, Fedorovsky M, et al. (2009) The Financial Bubble Experiment: Advanced Diagnostics and Forecasts of Bubble Terminations Volume Ⅱ -Assets Document. URL http://arXiv.org/abs/0911.0454. |

| [134] | Sornette D, Zhou W-X (2002) The us 2000-2002 market descent: How much longer and deeper? Quant Financ, 2: 468-481. |

| [135] | Sornette D, ZhouW-X (2004a) Evidence of fueling of the 2000 new economy bubble by foreign capital inflow: Implications for the future of the US economy and its stock market, . Phys A 332: 412-440. |

| [136] | Sornette D, Zhou W-X (2004b) Causal Slaving of the U.S. Treasury Bond Yield Antibubble by the Stock Market Antibubble of August 2000. Phys A 337: 586-608. |

| [137] | Sornette D, Woodard R, Zhou W-X (2009b) The 2006-2008 Oil Bubble and Beyond. Physica A 388: 1571-1576. |

| [138] | Stiglitz JE (1990) Symposium on bubbles. J Econ Perspect 4: 13-18. |

| [139] | Taipalus K (2012) Detecting asset price bubbles with time-series methods. Scientific monograph E 47, Helsinski. |

| [140] | The Closure and Subsequent Events. a. Available from: http://www.fstb.gov.hk/fsb/ppr/report/doc/DAVISON_E_APPENDIX.PDF. |

| [141] | The Gold Bubble. Available from: https://www.wealthmanagementinsights.com/userdocs/pubs/\QMU_The_Gold_Bubble__IMT_FINAL_8.15.11_TAGGED.pdf. |

| [142] | The observer, consumers go sour on the market's sugar rush, 2010. Available from: http://www.guardian.co.uk/business/2010/jan/31/sugar-prices-commodities. |

| [143] | Topol R (1991) Bubbles and volatility of stock prices: Effect of mimetic contagion. Econ J 101: 786-800. |

| [144] | Norden SV (1996) Regime switching as a test for exchange rate bubbles. J Appl Economet 11: 219-251. |

| [145] | Norden SV, Vigfusson R (1998) Avoiding the pitfalls: can regime-switching tests reliably detect bubbles? Stud Nonlinear Dyn E 2: 1-22. |

| [146] | Vogel HL, Werner RA (2015) An analytical review of volatility metrics for bubbles and crashes. Int Rev Financ Anal 38: 15-28. |

| [147] | Werner R (2005) The New Paradigm in Macroeconomics: Solving the Riddle of Japanese Macroeconomic Performance. Palgrave McMillan. |

| [148] | West K (1987) A specification test for speculative bubbles. Q J Econ 102: 553-580. |

| [149] | West K (1998) Bubbles, fads and stock price volatility tests: a partial evaluation. J Financ 43: 639-656. |

| [150] | Wu Y (1997) Rational bubbles in the stock market: accounting for the U.S. stock price volatility. Econ Inq 35: 309-319. |

| [151] | Xiong W(2013) Bubbles, Crises, and Heterogeneous Beliefs Handbook on Systemic Risk, Cambridge University Press 663-713. |

| [152] | Yang J, Bessler DA (2008) Contagion around the October 1987 stock market crash. Eur J Oper Res 184: 291-310. |

| [153] | Yao S, Luo D (2009) The Economic Psychology of Stock Market Bubbles in China. World Econ 32. |

| [154] | Zhang Q, Sornette D, Balcilar M, et al. (2016) LPPLS Bubble Indicators over Two Centuries of the S & P 500 Index. Physica A 458: 126-139. |

| [155] | Zhou WX, Sornette D (2003) The US2000-2003 market descent: Clarifications. Quantitative Financ 3: C39-C41. |

| [156] | Zweig J (2010) Back to the future: lessons from the forgoten 'flash crash' of 1962. Intell Invest. |

Figures(73) / Tables(1)

Didier Sornette, Peter Cauwels, Georgi Smilyanov. Can we use volatility to diagnose financial bubbles? lessons from 40 historical bubbles[J]. Quantitative Finance and Economics, 2018, 2(1): 486-590. doi: 10.3934/QFE.2018.1.1

DownLoad:

DownLoad: